High Yield Savings Account: The Complete Guide

The best high-yield savings accounts in 2026 pay 4%+ APY — up to 100x more than big banks. Here's how to pick the right one for your money.

Your big bank is paying you almost nothing. Chase, Wells Fargo, Bank of America — most of their standard savings accounts sit at 0.01% to 0.02% APY (rates change frequently — verify before opening). Park $10,000 there for a year and you'll earn somewhere between $1 and $2. Meanwhile, the best high yield savings accounts available right now are paying over 4% APY on that same balance — that's $400 in interest, no market risk, fully FDIC-insured.

The gap isn't small. It's the difference between a bank that works for you and one that works for itself. This guide ranks the best high-yield savings account options for 2026, with verified rates, honest pros and cons, and clear guidance on which one fits your situation. Whether you're building an emergency fund, stacking cash for a down payment, or just tired of watching your savings stagnate, there's a right account for you here.

Contents

- Ally Bank: Best All-Around HYSA

- Openbank: Best for a Clean High Rate

- American Express High Yield Savings: Best for Brand Trust

- Capital One 360 Performance Savings: Best for Existing Capital One Customers

- SoFi High Yield Savings: Best for Direct Deposit Bonuses

- Vio Bank: Best for Chasing the Highest Available Rate

- PNC High Yield Savings: Best for PNC Banking Customers

- Quick Comparison: All Picks at a Glance

- Watch This First

- What Real People Are Saying

- How We Chose These Accounts

- Common Questions

- Final Verdict

Ally Bank: Best All-Around HYSA

- Current APY: ~3.70% (PERMANENT, variable — verify on their site)

- Minimum opening deposit: $0

- Monthly fees: $0

- FDIC insurance: Standard $250,000 per depositor

- Unique feature: "Savings buckets" — multiple labeled sub-accounts within one savings account

Ally has been a go-to name in the HYSA space for well over a decade, and for good reason. No minimum balance. No monthly fees. A competitive rate that has consistently outpaced the national average. And a mobile app that doesn't make you want to throw your phone across the room.

The savings buckets feature is genuinely useful. Instead of opening five separate accounts to track your emergency fund, vacation fund, car repair fund, and down payment savings, Ally lets you create labeled buckets within one savings account. The money is all in one place for FDIC purposes, but your dashboard stays organized. It's the kind of small feature that actually changes behavior — when you can see "Emergency Fund: $8,400" in its own labeled bucket, you're less likely to dip into it for a spontaneous purchase.

Ally's rate isn't always the absolute highest on the market. You'll find accounts — particularly from smaller online banks — that post 10 to 30 basis points more. But Ally compensates with consistency, a polished interface, strong customer service, and zero conditions to earn the top rate. No direct deposit required, no minimum balance to maintain. You open the account and you earn the full posted APY from day one on any balance.

Transfer times are one area worth knowing about. Moving money between Ally and an external bank typically takes two to three business days, which is standard for online-only institutions. If you anticipate needing emergency access to funds same-day, keep a small float in a local checking account.

Pros

- No minimum deposit, no monthly fees — ever

- Savings buckets make goal-based saving genuinely practical

- Consistently competitive rate — no hoops to jump through

- Clean, intuitive mobile app with mobile check deposit

Cons

- Rate isn't always the highest available — rate chasers will find better elsewhere

- No physical branches — cash deposits aren't straightforward

- 2-3 day transfer lag to external accounts

Who It's For

Ally is the best default choice for most people — especially anyone who wants a reliable, fee-free account without having to chase promotional rates or meet conditions. It's ideal for emergency funds and goal-based savings. A good scenario: someone saving $500/month across three separate goals (emergency fund, new car, vacation) can use Ally's buckets to keep everything organized without opening multiple accounts at different banks.

Openbank: Best for a Clean High Rate

- Current APY: 4.00% (PERMANENT, variable — verify on their site)

- Minimum opening deposit: $500

- Monthly fees: $0

- FDIC insurance: Standard $250,000 per depositor

- Unique feature: Backed by Santander Bank — provides significant institutional backing for a digital-first product

Openbank is the online banking arm of Santander, one of the largest financial institutions in the world. That institutional backing matters when you're comparing lesser-known digital banks. The account itself is straightforward: 4.00% APY (rates change frequently — verify before opening) with no monthly fees, accessible as long as you open with at least $500.

That $500 minimum is the main friction point. It's not a dealbreaker for most people who are opening a high-yield savings account with meaningful money, but it does exclude someone who wants to park $200 while they build their balance. Once you're past that threshold, the account delivers cleanly. The rate is positioned well above the national average and doesn't require direct deposit, minimum balance maintenance, or any other hoops.

The digital experience is modern and functional. Openbank operates entirely online with no physical branch network, which is how they keep overhead low and pass the benefit on to depositors in the form of higher rates. The tradeoff is the same as with any online bank — transfers take a few business days, and cash deposits require some workaround.

For someone sitting on $5,000 in a big bank savings account earning virtually nothing, moving that balance to Openbank at 4.00% APY (rates change frequently — verify before opening) generates approximately $200 in interest over twelve months. That's real money that a traditional savings account simply does not pay. At a $10,000 balance, you're looking at $400 in annual interest — a meaningful return with zero investment risk.

Pros

- Highly competitive 4.00% APY (rates change frequently — verify before opening) with no conditions

- Backed by Santander — institutional credibility behind a digital product

- No monthly fees

Cons

- $500 minimum opening deposit

- No branch access

- Newer brand name in the U.S. Market — less name recognition than Ally or Amex

Who It's For

Openbank is an excellent choice for anyone who has at least $500 ready to deposit and wants a straightforward, high-rate account without promotional gimmicks. It's particularly well-suited to people who are comfortable with digital banking and want a rate that competes with the best on the market. If you're coming from a big bank savings account and have $1,000 or more to move, Openbank should be near the top of your list.

American Express High Yield Savings: Best for Brand Trust

- Current APY: Verify on their site — competitive with top-tier HYSAs

- Minimum opening deposit: $0

- Monthly fees: $0

- FDIC insurance: Standard $250,000 per depositor

- Unique feature: American Express brand trust and customer service reputation — one of the most recognized financial names in the country backing a no-fee savings product

American Express isn't just a credit card company. Their High Yield Savings Account has earned serious traction among people who want a competitive rate from a household name they already trust. The account requires no minimum opening deposit and carries no monthly maintenance fees — a clean, straightforward product from a company that has been in financial services for over 170 years.

For people who are skeptical about depositing thousands of dollars with a bank they've never heard of, American Express solves that problem immediately. You know the brand. You know the customer service reputation. That psychological comfort has real value, especially when you're moving your entire emergency fund somewhere new.

The account is available to anyone — you don't need to be an existing Amex cardholder to open it. The application process is fully online, and funds transfer in and out using standard ACH transfers. One thing to note: there's no ATM card and no checking account linked by default. This is a pure savings vehicle. That's a feature, not a bug — it creates natural friction against impulsive withdrawals, which helps emergency funds stay intact.

Amex's rate has been competitive with the top tier for much of the past few years, though it occasionally trails the absolute highest rates from smaller online banks. The trade is reliability and brand security over chasing an extra few basis points.

Pros

- No minimum deposit, no monthly fees

- Iconic brand trust — particularly valuable for first-time HYSA users

- No ATM card reduces temptation to raid savings

- Competitive rate with no conditions attached

Cons

- Rate occasionally trails top competitors by a few basis points

- No linked checking account or debit access

- No branch locations

Who It's For

American Express High Yield Savings is the best option for someone who values institutional trust above all else. If you're moving a six-month emergency fund — say $15,000 to $25,000 — and want it at a brand you implicitly trust, this is the account. It's also excellent for people who want natural friction to keep savings intact, since there's no debit card attached.

Capital One 360 Performance Savings: Best for Existing Capital One Customers

- Current APY: Verify on their site — competitive with major HYSA providers

- Minimum opening deposit: $0

- Monthly fees: $0

- FDIC insurance: Standard $250,000 per depositor

- Unique feature: Seamless integration with Capital One 360 Checking — instant internal transfers between checking and savings

Capital One's 360 Performance Savings account consistently surfaces in discussions about the best high-yield savings accounts for one core reason: if you're already a Capital One customer, the experience is frictionless. Moving money between a Capital One checking account and the savings account happens instantly — no two-to-three day ACH wait. For someone who wants high-yield rates while keeping their banking in one ecosystem, that's a compelling differentiator.

The account itself is genuinely competitive. No minimum to open, no monthly fees, and a rate that has kept pace with the major online banks. Capital One also offers physical café locations in select cities — a hybrid model that gives you the feel of a branch without the overhead that drags down traditional bank rates.

One scenario where this account shines: imagine you're self-employed and your income hits your Capital One checking account unevenly throughout the month. With 360 Performance Savings linked, you can immediately sweep excess cash into savings to earn high-yield rates, then pull it back to checking when a bill comes due — all without a multi-day transfer window eating into your liquidity.

Pros

- Instant internal transfers for existing Capital One checking customers

- No minimum deposit, no monthly fees

- Well-known, trusted bank with hybrid café branch model

- Strong mobile app

Cons

- Rate advantages are most significant if you're already in the Capital One ecosystem

- Rate occasionally trails the top online-only competitors

Who It's For

Existing Capital One customers, self-employed people who need fast liquidity between checking and savings, and anyone who values the convenience of a single-bank setup over chasing the absolute top APY available. Also a solid choice for first-time HYSA users who want a recognizable name.

SoFi High Yield Savings: Best for Direct Deposit Bonuses

- Current APY: Verify on their site — top rate typically requires direct deposit setup

- Minimum opening deposit: $0

- Monthly fees: $0

- FDIC insurance: Up to $2 million through a network of program banks (enhanced vs. Standard $250K)

- Unique feature: Enhanced FDIC coverage up to $2 million — the highest insurance limit on this list

SoFi's high-yield savings account has a caveat worth knowing upfront: the top APY is typically reserved for members who set up direct deposit. Without it, the rate drops meaningfully. If you can point your paycheck to SoFi — or if your employer allows split direct deposits so a portion goes there — you unlock the competitive rate and the full product.

The reason SoFi earns a spot on this list despite that condition is its FDIC coverage. SoFi offers up to $2 million in FDIC insurance by spreading deposits across a network of program banks. Standard FDIC coverage is $250,000 per depositor per bank. For most people saving $5,000 to $30,000, that distinction is irrelevant. But for someone sitting on a large cash position — an inheritance, proceeds from a home sale, or a business liquidity event — SoFi's enhanced coverage provides meaningful protection that most accounts don't offer.

SoFi has also been known for sign-up bonuses that can add up to several hundred dollars when you meet deposit thresholds. These promotions change, but they've been a recurring feature of SoFi's customer acquisition strategy. It makes SoFi particularly attractive for someone opening a new account with a significant initial deposit.

Pros

- Up to $2 million in FDIC insurance — best coverage on this list

- No monthly fees, no minimum deposit

- Potential sign-up bonuses for new members

- Full banking ecosystem — checking, savings, loans, investing in one app

Cons

- Top APY requires direct deposit — without it, rate is notably lower

- All-in-one app can feel cluttered if you only want savings

Who It's For

SoFi is the best pick for people who want enhanced FDIC coverage, can point a direct deposit to the account, or are opening with a large initial deposit to capture a sign-up bonus. High earners, business owners, or anyone with more than $250,000 in cash savings will find SoFi's coverage limit especially valuable.

Vio Bank: Best for Chasing the Highest Available Rate

- Current APY: Among the top in the market — consistently cited among leaders at 4%+ (verify on their site)

- Minimum opening deposit: $100

- Monthly fees: $0

- FDIC insurance: Standard $250,000 per depositor

- Unique feature: Consistently ranks among the absolute highest rates nationwide — not promotional, this is their permanent competitive position

Vio Bank is the online division of MidFirst Bank, one of the largest privately held banks in the United States. That institutional backing is often overlooked because Vio operates entirely online with minimal marketing. But it's important — MidFirst has been operating since 1911, which means Vio's competitive rates come from a bank with deep, established infrastructure, not a startup burning through venture capital to acquire customers.

Vio's primary appeal is its rate. It regularly ranks among the highest available nationwide, with a $100 minimum to open. No monthly fees, straightforward terms. For someone who tracks high-yield savings account rates and moves their money to maximize yield, Vio is the kind of account worth monitoring closely.

The tradeoff: Vio is a no-frills operation. The interface is functional but not polished. There's no full banking ecosystem — no checking account, no investment accounts, no app features beyond what you need for savings. If you need your savings account to be part of a broader financial hub, Vio isn't that. But if your goal is pure yield with a low minimum and no fees, Vio consistently delivers.

Consider this scenario: you have $20,000 in a standard savings account at 0.01% APY (rates change frequently — verify before opening) earning $2 per year. Moving it to Vio at 4%+ APY generates $800 or more annually. That's not a rounding error — that's a car payment, a plane ticket, or a meaningful chunk of an emergency fund built purely from interest your money was already earning somewhere else for almost nothing.

Pros

- Consistently among the highest APYs available

- Backed by established MidFirst Bank — not a startup

- Low $100 minimum opening deposit

- No monthly fees

Cons

- Basic app and digital interface — not a premium experience

- No checking account or broader banking ecosystem

- Lower brand recognition may cause hesitation

Who It's For

Rate-focused savers who want the highest APY available and don't need their savings account to do anything fancy. If you're comfortable managing your day-to-day banking elsewhere and just want maximum yield on parked cash, Vio Bank belongs on your shortlist.

PNC High Yield Savings: Best for PNC Banking Customers

- Current APY: 3.25% APY (rates change frequently — verify before opening) (verify on their site)

- Minimum opening deposit: $0

- Monthly fees: $0

- FDIC insurance: Standard $250,000 per depositor

- Unique feature: Offered by a major traditional bank with 2,200+ branches nationwide — rare combination of high-yield rate and physical branch access

Most high-yield savings accounts come from online-only banks with no physical presence. PNC breaks that pattern. With over 2,200 branches across the country, PNC's High Yield Savings account at 3.25% APY (rates change frequently — verify before opening) offers something the other picks on this list can't: in-person service when you need it.

The rate at 3.25% is lower than Openbank or Vio Bank, but it's dramatically higher than the standard savings rates PNC customers would otherwise earn — and it's competitive with many top-tier online banks. For existing PNC customers who don't want to move their banking relationship, this account gives them access to above-average yield without leaving their bank.

No minimum balance and no monthly fees keep it clean. The account is designed to complement PNC's existing product lineup, so integration with checking and other PNC products is seamless. For someone who relies on branch access — for cash deposits, in-person questions, or notary services — PNC offers a rare hybrid: meaningful yield with physical backup.

Pros

- Significant branch network — best physical access of any pick on this list

- No minimum balance, no monthly fees

- Well above national average APY

- Seamless integration with PNC checking

Cons

- Rate trails top online-only competitors by 0.50%+ in some cases

- Best for PNC existing customers — switching banks just for this account may not maximize value

Who It's For

Existing PNC customers who want to earn more without switching banks, and anyone who still values branch access and isn't willing to sacrifice it entirely for yield. Also worth considering for people in PNC-heavy markets (Mid-Atlantic, Southeast, Midwest) who want local banking with above-average savings rates.

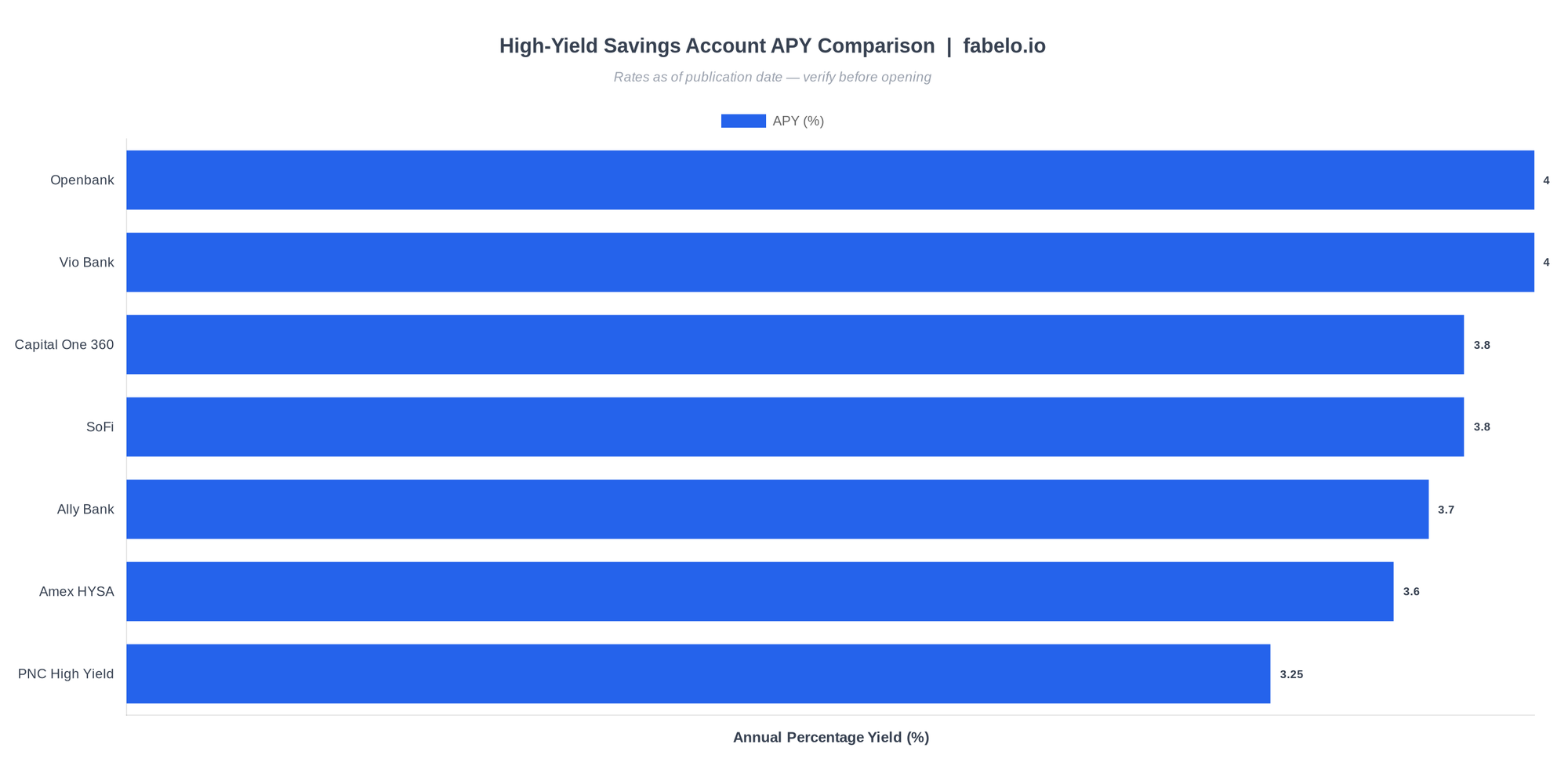

Quick Comparison: All Picks at a Glance

| Bank | APY | Min. Deposit | Monthly Fee | FDIC Coverage | Best For |

|---|---|---|---|---|---|

| Ally Bank | ~3.70%* | $0 | $0 | $250K standard | All-around best; goal-based saving |

| Openbank | 4.00%* | $500 | $0 | $250K standard | Clean high rate, no conditions |

| American Express HYSA | Verify on site* | $0 | $0 | $250K standard | Brand trust, no-debit savings |

| Capital One 360 | Verify on site* | $0 | $0 | $250K standard | Existing Capital One customers |

| SoFi | Verify on site* | $0 | $0 | Up to $2M enhanced | Direct deposit + large balances |

| Vio Bank | 4%+ range* | $100 | $0 | $250K standard | Rate chasers, yield maximizers |

| PNC High Yield | 3.25%* | $0 | $0 | $250K standard | PNC customers, branch lovers |

*Rates change frequently — verify current APY directly with each institution before opening an account.

Watch This First

Before you open anything, this video from FIRE Psy Chat cuts through the typical HYSA noise with a decade of real personal experience. The core insight worth internalizing: the reason online banks consistently outpay traditional banks has nothing to do with gimmicks. Online institutions simply don't carry the overhead costs of thousands of physical branches — no rent, no security guards, no landscaping for 5,000 locations — and they pass those savings directly to depositors as higher APY. According to FIRE Psy Chat, even during the low-rate environment of 2019 and 2020, their HYSA was still paying more than 10 times what a traditional big bank savings account offered. That yield gap is structural, not temporary.

The video also makes a point that often gets buried in rate comparisons: look for daily compounding. A rate that compounds daily grows faster than the same rate compounding monthly or quarterly, even if the posted APY looks identical. It's a small but real difference that adds up over years of consistent saving. Watch the full breakdown here: Watch: the FIRE Psy Chat YouTube channel — Best HYSAs for 2026 →

What Real People Are Saying

Reddit's personal finance community has been vocal about HYSAs for years, and the consensus is clearer than you might expect. In r/personalfinance, users consistently point to Ally Bank, Capital One 360, and American Express as the go-to starting points — all described as solid, no-fee, FDIC-insured accounts that don't require you to navigate complex conditions to earn the top rate. The general sentiment: if you're just getting started with HYSAs, these names are safe ground.

The transaction limit question comes up repeatedly in r/HighYieldSavings. Several users note that while Ally is broadly loved, its withdrawal limitations are a real friction point for people who move money frequently. The practical workaround that experienced users recommend: keep a small buffer in a checking account at your regular bank so you're not constantly reaching into savings for day-to-day needs.

On the question of how much to keep in a regular savings account versus a high-yield one, users in r/personalfinance offer a straightforward framework: keep a small buffer — often one to two weeks of expenses — in your local checking account for immediate access, and move everything else to a HYSA earning 3% or better. As one commenter put it directly: anything beyond that buffer belongs in a high-yield account, period. The math isn't complicated. A traditional savings account paying under 0.10% isn't keeping up with inflation. A HYSA at 3% to 4%+ at least gives your cash a fighting chance.

How We Chose These Accounts

Every account on this list was evaluated against the same set of criteria. Rate alone doesn't win a spot. A 4.50% promotional APY that drops to 0.50% after 90 days is worse for most people than a consistent 3.80% permanent rate. We weighted consistency, transparency, and practical usability heavily alongside headline APY.

Here's the framework used to build this list:

| Criteria | What We Looked For |

|---|---|

| APY — Rate Quality | Permanent vs. Promotional rate. Rate must meaningfully beat the national average savings rate without expiring in 60-90 days. |

| Fees | $0 monthly maintenance fees required. Accounts with hidden fees or balance requirements that trigger fees were excluded. |

| Minimum Deposit | Noted clearly for every pick. Accounts with high minimums ($5,000+) to earn the top rate were excluded unless they offered exceptional value elsewhere. |

| FDIC / NCUA Insurance | All picks are fully insured. Enhanced coverage (like SoFi's $2M limit) noted where applicable. |

| Rate Conditions | Accounts requiring direct deposit or minimum balance to earn the advertised rate are flagged clearly. Unconditional rates scored higher. |

| Usability | Mobile app quality, ease of account setup, customer service reputation, and transfer experience all factored in. |

| Institutional Stability | Newer fintech startups with uncertain long-term viability were excluded. Every pick is either a major bank or backed by established banking infrastructure. |

What we excluded — and why. Several accounts with eye-catching promotional rates didn't make the list. If the rate is advertised for a limited introductory period and then drops significantly, that's a bait-and-switch dynamic that penalizes anyone who doesn't obsessively track their APY. We also excluded accounts that require you to jump through multiple conditions simultaneously — minimum balance, direct deposit, and minimum number of monthly transactions — just to earn the stated rate. The best high-yield savings account for most people is one that pays a strong rate without requiring you to actively manage it like a checking account.

Rates in this article reflect what was available from public sources at time of writing. Rates change frequently — verify current APY before opening any account.

Common Questions

How much can $10,000 make in a high-yield savings account?

At 4.00% APY (rates change frequently — verify before opening), $10,000 grows to approximately $10,400 after one year — that's $400 in interest earned with zero investment risk. For comparison, a national average savings account at around 0.60% would return roughly $60 on the same balance, and a big bank savings account at 0.01% would earn about $1. The difference compounds over time: over three years at 4.00% APY (rates change frequently — verify before opening), that $10,000 grows to roughly $11,249. The math is simple and the gap is large. (Rates change frequently — verify current APY before opening.)

What happens if I put $5,000 in a high-yield savings account?

At 4.00% APY (rates change frequently — verify before opening), $5,000 generates approximately $200 in interest over one year. After two years with no additional contributions, the balance grows to around $5,408 through compounding. After five years, you're looking at roughly $6,083 — all without touching the market. If you add $200/month on top of the initial $5,000, the math improves dramatically. Use a high-yield savings account calculator to model your specific scenario based on your balance and contribution plan. (Rates change frequently — verify current APY before opening.)

Are the rates permanent or promotional?

Most of the accounts on this list offer permanent variable rates — meaning the rate moves with the Federal Reserve's decisions, not with an arbitrary promotional clock. Variable rates will fluctuate over time, but they're not set to drop to 0.50% after 90 days the way some promotional offers are structured. A few institutions do offer promotional introductory rates that are time-limited. Always read the fine print and look for the word "promotional" in any rate disclosure. If it's not explicitly labeled as permanent, ask the bank directly before you transfer your savings.

Is my money safe in a high-yield savings account?

Yes — every account on this list is either FDIC-insured (if bank-based) or NCUA-insured (if credit union-based) up to at least $250,000 per depositor. That insurance is backed by the U.S. Federal government. Even if the bank failed, your deposits up to the coverage limit would be protected. SoFi offers enhanced coverage up to $2 million through a program bank network for those with larger balances. For the vast majority of savers, standard $250,000 FDIC coverage is more than sufficient.

What are the alternatives to a high-yield savings account?

Three worth knowing: Treasury money market funds like SGOV (iShares 0-3 Month Treasury Bond ETF) or VUSXX (Vanguard Treasury Money Market Fund) often yield comparably to HYSAs and may offer state tax advantages on interest. Brokerage cash accounts at firms like Fidelity or Schwab can also offer competitive rates on uninvested cash. Certificates of deposit (CDs) lock your money for a set term — typically 3 to 24 months — in exchange for a guaranteed rate, which can be higher than a HYSA if you don't need liquidity. For money you won't touch for 12+ months, a CD ladder is worth exploring alongside your HYSA.

Can I use a high-yield savings account calculator to estimate my earnings?

Absolutely, and you should. A high-yield savings account calculator takes your starting balance, monthly contribution, APY, and time horizon and outputs your projected earnings. Most major financial sites offer free calculators. The key variable to watch is contribution frequency — adding even $100 a month to a $5,000 starting balance at 4.00% APY (rates change frequently — verify before opening) produces dramatically different results than leaving the balance static. Run your actual numbers before you decide which account makes the most sense for your goals.

Should I keep any money in a traditional savings account?

Keep a small operational buffer — one to two weeks of expenses — in a local checking account for immediate access and ATM withdrawals. Beyond that, there's almost no financial reason to park cash in a traditional savings account paying 0.01% to 0.02% APY (rates change frequently — verify before opening). The practical move: use a HYSA as your primary savings vehicle and a traditional checking account for day-to-day spending. That structure gives you high yield on your parked cash and full liquidity for your daily needs.

Final Verdict

Our top pick: Ally Bank. Not because it always has the highest rate in the market — it doesn't. It wins because it reliably delivers a competitive APY with zero fees, zero minimum deposit, and genuinely useful features like savings buckets that make goal-based saving practical. For most people — whether you're building a three-month emergency fund, saving for a down payment, or just tired of your big bank paying you next to nothing — Ally is the cleanest starting point.

If your only criterion is maximum APY and you're comfortable with a no-frills digital experience, Vio Bank and Openbank belong at the top of your list. If you have a large cash position above $250,000, SoFi's enhanced FDIC coverage is a genuine differentiator worth factoring in. And if you're an existing PNC or Capital One customer who doesn't want to switch banks entirely, both offer above-average rates without forcing you to leave your current financial setup.

Bottom line: A high yield savings account is the simplest upgrade most Americans can make to their finances right now. The accounts exist, the rates are real, and every dollar sitting in a big bank savings account at 0.01% is a dollar that could be earning 40 times more somewhere else. Pick one from this list, verify the current rate, and move your money. The gap between doing nothing and doing this is measured in hundreds of dollars per year.

Your three-step action plan:

- Decide how much you want to move and whether you have direct deposit flexibility (if yes, SoFi becomes a stronger option).

- Check current APYs at Ally, Openbank, and your bank of choice on the day you're ready to open — rates move and yesterday's leader isn't always today's.

- Open the account, set up an automatic transfer from checking, and let your savings earn what they should have been earning all along.

About the Author

Written by Varn Kutser

Personal finance writer focused on savings, budgeting, and building wealth at Fabelo.io. Cuts through the noise to find accounts that actually earn.

Disclaimer: Rates and terms mentioned in this article are subject to change. Verify current rates directly with financial institutions before opening any account.

Last updated: April 11, 2026 · fabelo.io