Debt Consolidation Loan Bad Credit: The Complete Guide

Bad credit doesn't mean you're out of options. This guide covers how to get a debt consolidation loan with bad credit, which lenders to consider, and what

Bad credit and debt is a brutal combination. You need relief from high-interest balances, but the very thing dragging your credit score down — those same balances — makes it harder to qualify for the loan that could help. It feels circular, and for a lot of people, it is. But lenders who work with bad credit borrowers do exist, and your options are wider than most people realize.

A debt consolidation loan for bad credit works the same way as any consolidation loan: you borrow a lump sum, pay off your existing balances, and make a single monthly payment at (ideally) a lower interest rate. The difference is that with a credit score in the 500s or low 600s, you'll face higher rates, lower loan limits, and stricter income requirements. That doesn't make it pointless — even moving from a 28% credit card APR to a 20% personal loan can save you hundreds per year and dramatically simplify your finances.

This guide covers how the process actually works, which lenders are worth your time, what "guaranteed approval" really means, how to get a debt consolidation loan bad credit no collateral, and the red flags that signal you're about to get taken advantage of. By the end, you'll know exactly what to do — and what to avoid.

All rates and APRs mentioned in this article are for illustration purposes. Rates change frequently — always verify current rates directly with the lender before applying.

Contents

- What Bad Credit Actually Means for Consolidation Loans

- Where to Find a Debt Consolidation Loan Bad Credit Borrowers Can Qualify For

- Debt Consolidation Loan Bad Credit No Collateral: How It Works

- The Truth About "Guaranteed Approval" Offers

- How to Strengthen Your Application Before You Apply

- Alternatives When a Loan Isn't the Right Move

- Comparison Table: Debt Consolidation Options for Bad Credit

- Watch This First

- What Real People Are Saying

- Frequently Asked Questions

- Your Next Steps

What Bad Credit Actually Means for Consolidation Loans

Credit scores in the United States are typically measured on the FICO scale from 300 to 850. "Bad credit" generally refers to scores below 580, though lenders vary on where they draw the line. Scores between 580 and 669 are considered "fair" — still a challenging range for most traditional bank products. If you're sitting at a 520 or a 601, you're not in impossible territory, but you do need to know where to look.

Here's what bad credit concretely costs you in a consolidation loan scenario. A borrower with a 720+ score might qualify for an APR in the 10–14% range. Someone with a 580 score at the same lender might see 24–30%. At 520, you're potentially looking at 30–36% — which is the legal maximum for most personal loan lenders. At that point, you have to do the math carefully. If your existing credit card debt is already at 29.99%, a consolidation loan at 34% doesn't help you. It just moves the debt around.

That math matters more than people think. The goal isn't just simplification — it's saving money. If a consolidation loan doesn't lower your effective interest rate, it's not solving your problem. However, even at similar rates, the fixed repayment schedule of a personal loan has real value: your balance actually goes down every month on a predictable timeline, unlike revolving credit card debt where minimum payments can keep you trapped for a decade.

Lenders evaluate bad credit borrowers on more than just the score. Debt-to-income ratio (DTI) is often equally important. If you bring home $4,000 a month and your monthly debt obligations total $1,500, your DTI is 37.5%. Most lenders want to see that figure below 40–45%, though some bad credit lenders push that ceiling higher. Steady employment history and verifiable income matter a lot — lenders want evidence you can repay, even when your past record shows you've struggled.

One practical point: a single hard inquiry from a loan application typically drops your credit score by about five points. If you're applying to multiple lenders in a short window — say, within 14–30 days — FICO typically treats those as a single inquiry for rate-shopping purposes. Use this to your advantage. Apply to several lenders simultaneously rather than one at a time, and use pre-qualification tools that only require a soft pull first.

Where to Find a Debt Consolidation Loan Bad Credit Borrowers Can Qualify For

The best debt consolidation loans for bad credit don't come from the same places a 750-score borrower would look. You need lenders built for this situation — or at least lenders with genuinely flexible underwriting. Here's where to focus your search.

Credit Unions

Credit unions are consistently the most underused resource for bad credit borrowers. Because they're member-owned nonprofits, they're not chasing profit margin on every loan — they're serving their members. That means they often have more flexible credit requirements, lower rate caps, and a genuine willingness to look at the full picture rather than just your score.

In r/povertyfinance, users consistently recommend Navy Federal Credit Union, noting that they consider your overall financial profile rather than just the credit score — and offer personal loans from $250 up to $50,000. If you're not military-affiliated, many federal credit unions have easy membership criteria: some require only a small donation to a partner organization or that you live in a certain area. It's worth spending 15 minutes checking eligibility before writing off this category.

Truliant Federal Credit Union, for example, offers debt consolidation loans with fixed rates and immediate pre-qualification that doesn't require a hard pull. That's the kind of transparency worth seeking out.

Online Lenders and Lending Marketplaces

Online lenders have fundamentally changed the bad credit lending landscape. Companies like Achieve, Prosper, and LendingTree's network operate with lower overhead than traditional banks, and some specialize specifically in non-prime borrowers.

Achieve offers three distinct paths: a personal loan, a home equity loan, and a debt relief program. The personal loan route requires no collateral and is designed specifically for people consolidating multiple debts. Their underwriting considers your full financial picture, not just the score.

LendingTree functions as a marketplace — you submit one application and receive offers from multiple lenders simultaneously. Their data shows that bad credit users receive an average of five or more loan offers when they apply, giving you genuine comparison power without multiple hard inquiries upfront.

Prosper specializes in credit card debt consolidation specifically, with flexible payment terms and no prepayment penalties — meaning you can pay it off early without getting penalized for it, which matters if your financial situation improves.

Debt Consolidation Loan Bad Credit Direct Lender Options

Working with a debt consolidation loan bad credit direct lender — rather than a broker or marketplace — can streamline the process and sometimes result in better terms, because there's no intermediary taking a cut or steering you toward a higher-rate product. Direct lenders also give you a single point of contact for any issues that arise during the loan term.

The tradeoff is that you get one offer per application. Using a marketplace first to understand what rates you qualify for, then going directly to your preferred lender for the formal application, is often the smartest sequence. Discover, for instance, offers personal loans up to $40,000 for debt consolidation with fixed rates and no origination fees — a significant advantage since origination fees on bad credit loans can run 1–8% of the loan amount.

Avoid Payday and "No Credit Check" Lenders

There's a category of lenders aggressively marketing to people in financial distress, and they deserve explicit warning. Payday lenders, some tribal lenders, and "no credit check" loan shops frequently charge effective APRs in the triple digits — sometimes 300% or more. A "debt consolidation loan bad credit no credit check" from one of these sources will almost certainly make your situation worse. If a lender genuinely doesn't check your credit at all, they're pricing the risk into the rate — and that price is often catastrophic.

Debt Consolidation Loan Bad Credit No Collateral: How It Works

Most people searching for debt consolidation don't have a home or significant assets to pledge as collateral — and shouldn't have to. The good news is that most personal loans used for debt consolidation are unsecured, meaning a debt consolidation loan bad credit no collateral is the standard product, not a special exception.

An unsecured personal loan means the lender is extending credit based on your creditworthiness and income alone. There's no car title, no house deed, no savings account pledge. If you default, the lender can pursue you legally, but they can't automatically seize your assets the way a secured creditor can. That's meaningful protection for borrowers who are already financially vulnerable.

Because the lender takes on more risk with an unsecured loan, the rates are higher than secured alternatives. But compare the options:

- Home equity loan or HELOC: Often the lowest rates, but you're putting your home on the line. Miss payments and you can lose your house. For someone with bad credit and debt problems, this is high-stakes collateral.

- Secured personal loan: You pledge a savings account or CD. Lower rate, but you're locking up liquid assets you might need.

- Unsecured personal loan: Higher rate, but no asset risk. You keep your collateral intact.

For most bad credit borrowers carrying $5,000–$20,000 in credit card or personal loan debt, the unsecured route is the appropriate path. The rate will be higher than ideal, but the structure is cleaner and safer given the circumstances.

Loan amounts on unsecured bad credit consolidation products typically range from $1,000 to $25,000, though some lenders go higher. Repayment terms usually span 24 to 60 months — and longer terms mean smaller monthly payments but more interest paid overall. A $10,000 loan at 25% APR over 36 months costs you roughly $4,200 in interest. Extend that to 60 months and the payment drops, but the total interest paid jumps to around $7,500. Run those numbers before you commit to a term.

The Truth About "Guaranteed Approval" Offers

Searches for "debt consolidation loan bad credit guaranteed" spike every year, and it's easy to understand why. When you're in financial distress and have been rejected by multiple lenders, the promise of guaranteed approval feels like a lifeline. Here's the reality: no legitimate lender can guarantee approval before reviewing your application.

A lender that promises "guaranteed approval" before knowing your income, your debt load, your identity, or your repayment history isn't underwriting loans — they're marketing. What often follows are extremely high-rate loans with short terms, excessive fees, or outright scams where you pay an upfront "processing fee" and receive nothing in return.

What legitimate lenders do offer is "pre-qualification" — a soft credit pull that gives you a rate estimate without affecting your score. That's genuinely useful. It's not guaranteed approval, but it tells you what range you're likely to qualify for before you formally apply. Most reputable online lenders and credit unions offer this. If a lender won't pre-qualify you and instead pushes you straight to a full application promising approval, that's a red flag.

Real approval criteria for bad credit personal loans usually include:

- Minimum credit score (often 560–580 for many online lenders)

- Verifiable income — typically $1,500–$2,000/month minimum

- Active bank account in good standing

- Debt-to-income ratio below the lender's threshold

- No recent bankruptcies (some lenders will work with discharged bankruptcies after 1–2 years)

If you don't meet a lender's published criteria, the responsible move is to work on one or two of those variables — not to chase "guaranteed" offers that don't exist from legitimate sources.

How to Strengthen Your Application Before You Apply

Even a modest improvement in your profile before you apply can meaningfully change the outcome — either by qualifying you for a lender who previously wouldn't touch you, or by securing a lower rate that saves you real money over the loan term.

Check All Three Credit Reports for Errors

Federal law entitles you to a free credit report from each bureau (Equifax, Experian, TransUnion) annually at AnnualCreditReport.com. Errors are more common than most people expect — incorrect balances, accounts that don't belong to you, duplicate derogatory marks. Disputing and removing legitimate errors can raise your score meaningfully in 30–60 days, sometimes by 20–40 points, without paying anyone anything.

Add a Co-Signer

If you have a trusted family member or close friend with good credit, a co-signer can transform your application. The lender considers the co-signer's credit profile alongside yours, which can unlock significantly better rates and higher loan limits. The risk for the co-signer is real — if you default, they're legally responsible — so this arrangement requires genuine trust and a clear repayment plan you both understand.

Reduce Your Credit Utilization Before Applying

Credit utilization — the ratio of your balances to your credit limits — is one of the most significant scoring factors. If you have $5,000 in credit card limits and $4,500 in balances, your utilization is 90%, which hammers your score. Paying down even $1,000–$1,500 before applying can drop utilization below 70% and nudge your score upward. Time the application for right after that payment is reflected on your report.

Document Your Income Thoroughly

Bad credit lenders lean hard on income verification. Have your last two pay stubs, two months of bank statements, and your most recent W-2 ready. If you're self-employed or have gig income, two years of tax returns are typically required. Lenders in this space get burned by borrowers who look good on paper but have unstable income — showing consistent, verifiable cash flow makes you a far more compelling applicant.

Lower Your Loan Request

There's a counterintuitive strategy here: ask for less. If your debt totals $15,000 but you can reasonably pay $5,000 off yourself over the next few months, consolidate the remaining $10,000. A smaller loan request improves your approval odds and your rate. You can always pay extra toward the remaining balances separately.

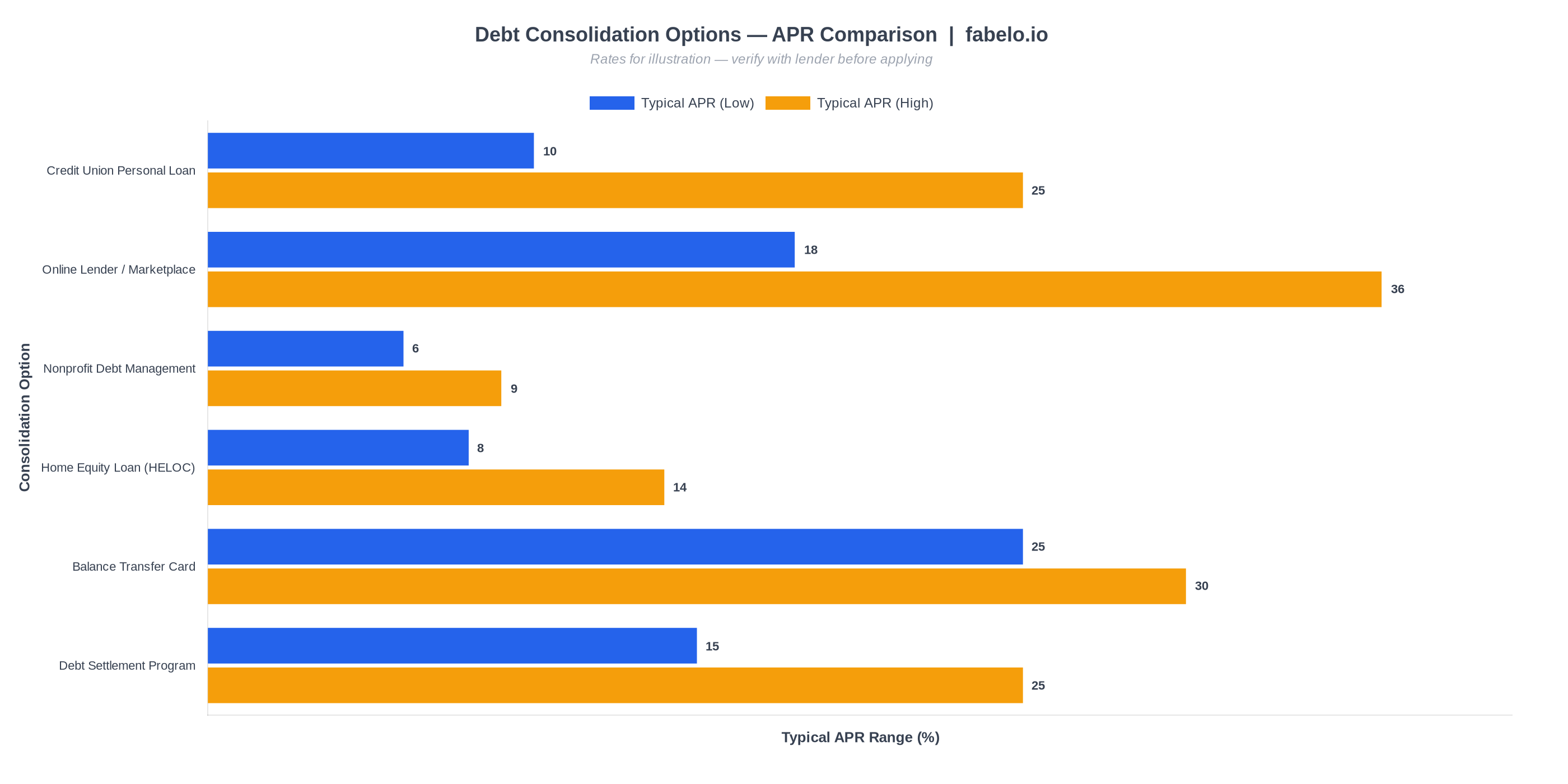

| Option | Typical APR Range | Collateral Required? | Min. Credit Score | Best For |

|---|---|---|---|---|

| Credit Union Personal Loan | 10–25% (verify directly) | No | ~560+ | Members with steady income despite low scores |

| Online Lender / Marketplace | 18–36% (verify directly) | No | ~560–580+ | Comparing multiple offers quickly |

| Nonprofit Debt Management Plan | 6–9% (negotiated) | No | None required | Anyone who can't qualify for a personal loan |

| Home Equity Loan (HELOC) | 8–14% (verify directly) | Yes (your home) | ~620+ | Homeowners with equity who understand the risk |

| Balance Transfer Card | 0% promo, then 25–30% | No | ~580–620+ | Smaller balances payable within 12–18 months |

| Debt Settlement Program | N/A (fee-based: 15–25% of debt) | No | None required | Severely delinquent borrowers as a last resort |

Alternatives When a Loan Isn't the Right Move

A personal loan isn't the only path to debt relief. Sometimes it's not even the best one. Before committing, evaluate these alternatives against your specific situation.

Nonprofit Credit Counseling and Debt Management Plans

Accredited nonprofit credit counseling agencies — look for NFCC-member organizations — can set you up on a Debt Management Plan (DMP). In a DMP, the agency negotiates reduced interest rates directly with your creditors, sometimes getting rates down to 6–9% even on existing high-rate credit card debt. You make one monthly payment to the agency, which distributes it. You don't need good credit to qualify, and there's no new loan involved. The downside: it takes 3–5 years, and you typically can't use credit cards during the plan.

Balance Transfer Cards for Fair Credit

If your credit score is on the higher end of the "bad" range — say, 580–650 — some issuers offer balance transfer cards with 0% promotional periods of 12–18 months. The transfer fee is typically 3–5% of the balance, but if you can pay off the debt within the promotional window, you're effectively getting an interest-free loan for a year or more. This works best for smaller balances ($2,000–$5,000) that you have realistic cash flow to eliminate quickly.

Negotiate Directly With Creditors

This is underused and often surprisingly effective. If you're behind on payments, creditors may offer hardship programs, reduced settlement amounts, or temporarily lowered rates. A single phone call to each creditor, explaining your situation and asking for options, can yield results. Creditors often prefer a modified payment arrangement to the expense of a collections process.

Debt Settlement

Achieve and similar companies offer debt relief (settlement) programs as an alternative to a personal loan. In debt settlement, you stop paying creditors and accumulate funds in a dedicated account, then negotiate lump-sum settlements for less than you owe. This is a legitimate strategy for people who are already severely delinquent and can't qualify for any loan — but it comes with serious credit score damage and potential tax consequences on forgiven debt. It's a last resort, not a first move.

Comparison Table: Debt Consolidation Options for Bad Credit

Rates are illustrative ranges based on publicly available lender information. Verify current terms directly with each lender or program before applying.

Watch This First

Before you submit any application, spend a few minutes watching this breakdown of personal loan options for bad credit borrowers: Watch: Best Loans for Bad Credit of 2026 →

The Brennan Valeski YouTube channel covers several loan marketplaces worth knowing about. One practical point emphasized is the value of submitting your information to multiple platforms simultaneously — not just one — because rates and terms vary significantly across lenders and there's no obligation to accept any offer. The channel highlights that even for borrowers with very low scores, funding can arrive within one business day at some lenders, which matters when you're dealing with urgent balances. The video also flags that some platforms offer rates as high as 35.99%, which underscores why comparison-shopping isn't optional — it's the only way to avoid landing on the worst end of the range.

This is especially relevant for anyone chasing a debt consolidation loan bad credit direct lender: even direct lenders benefit from being compared against marketplace offers first, so you arrive at the negotiating table knowing what the competitive rate actually looks like for your profile.

What Real People Are Saying

The most useful real-world perspective on bad credit consolidation loans comes from people who've actually tried — not from marketing copy. Across several Reddit communities, the pattern is consistent and worth paying attention to.

In r/povertyfinance, users navigating sub-600 credit scores repeatedly point to credit unions as the most realistic first stop — specifically noting that lenders like Navy Federal look at employment history and income stability rather than treating the credit score as a hard cutoff. The common thread: people who get approved aren't necessarily people with better credit, they're people who can demonstrate consistent income even if past payments have been a problem.

In r/personalfinance, one user asked about options for a family member carrying over $10,000 in debt at a 526 credit score — a scenario many people find themselves in. The community response was clear: at that score, traditional banks are largely off the table, but online lenders that use alternative underwriting criteria, credit unions with flexible membership requirements, and nonprofit debt management programs are all realistic paths. The advice to "show proof of income and don't be afraid to explain your situation" came up multiple times.

In r/Debt, users emphasize a reality that doesn't get enough attention: the rate you qualify for with bad credit might not actually lower your cost of borrowing. More than one commenter recommended running the numbers — specifically calculating total interest paid under the consolidation loan versus continuing minimum payments on existing debt — before committing. That's exactly the right framework. A debt consolidation loan bad credit situation requires mathematical justification, not just emotional relief.

Frequently Asked Questions

Can I get a debt consolidation loan with a 520 credit score?

Yes, but your options narrow significantly below 580. At a 520, most traditional banks and credit unions will decline you. Your realistic paths are online lenders that use alternative underwriting — looking at income, employment history, and bank account health rather than score alone — or a nonprofit debt management plan that doesn't require a credit check at all. Some marketplace lenders also work with scores in this range. Expect rates at the higher end (25–36%) if you do qualify. Be honest with yourself about whether the rate actually helps your situation before borrowing.

What does "no collateral" mean for a debt consolidation loan?

A no-collateral loan — also called an unsecured loan — means the lender isn't requiring you to pledge a specific asset (like your car or home) to secure the debt. If you default, the lender can sue you and potentially garnish wages or bank accounts through the courts, but they can't automatically repossess an asset. Most personal loans used for debt consolidation are unsecured. This is generally the safer structure for borrowers who are already financially stretched, even though rates are higher than secured alternatives.

Is there really such a thing as a guaranteed debt consolidation loan for bad credit?

No legitimate lender guarantees approval before reviewing your application. Any company advertising "guaranteed" consolidation loans — especially online — should be approached with serious skepticism. Real pre-qualification exists (soft pull, no commitment), and that's useful. But a guarantee before any underwriting is a marketing claim, not a financial reality. The actual scam risk here is real: some operations collect "processing fees" upfront and deliver nothing. Never pay money to apply for a loan from a consumer lender.

How long does it take to get a debt consolidation loan with bad credit?

With online lenders, the timeline is often surprisingly fast. Pre-qualification can happen in minutes. Full approval after document submission typically takes 1–3 business days for most online and marketplace lenders. Funding — once you accept an offer and sign documents — often arrives within one business day. Credit unions can be slower, sometimes taking a week or more if they require in-person verification. If speed matters (you have a payment due imminently), online lenders are the faster route.

Will applying for a consolidation loan hurt my credit score?

Pre-qualification with a soft pull won't affect your score at all. A formal application triggers a hard inquiry, which typically causes a temporary 5-point drop. If you apply to multiple lenders within a 14–30 day window, FICO typically treats the multiple hard inquiries as a single event for scoring purposes — a policy designed specifically for rate-shopping. Longer term, if you're approved and you make on-time payments, the loan can actually help your score by improving your payment history and reducing your overall credit utilization (by paying off revolving balances).

What's the difference between a debt consolidation loan and debt settlement?

A debt consolidation loan is a new loan you use to pay off existing debts — you still owe the full amount, just to a new lender at (hopefully) better terms. Debt settlement involves negotiating with creditors to accept less than the full amount owed, usually after you've fallen behind. Settlement is more damaging to your credit score and may result in taxable "forgiven debt" income. Consolidation is the better option for people who can still make payments; settlement is more appropriate as a last resort for severely delinquent borrowers who truly cannot repay the full balance.

Your Next Steps

Getting a debt consolidation loan with bad credit requires a clear-eyed strategy — not hope, not desperation, and definitely not "guaranteed approval" lenders. Here's the specific action plan that makes sense given everything covered above.

- Pull your credit reports first. Go to AnnualCreditReport.com and review all three bureau reports for errors before you apply anywhere. Dispute inaccuracies and give them 30 days to resolve. This is free and can move your score meaningfully before any lender sees it.

- Pre-qualify at a lending marketplace and at least one credit union simultaneously. Use a marketplace like LendingTree to see multiple offers with a single soft pull, and separately check with a credit union you're eligible to join. Compare the rate, term, fees, and total cost — not just the monthly payment.

- Run the total interest math before you sign anything. Calculate what you'll pay in total interest over the loan term versus what you'd pay continuing on your current trajectory. If the consolidation loan saves you money and simplifies your repayment — proceed. If it doesn't lower your rate meaningfully, explore a nonprofit debt management plan through an NFCC-member counselor instead.

Debt consolidation with bad credit is a real option, not a fantasy. But it requires discipline about which offers you accept and honesty about whether the numbers actually work in your favor. The right move depends on your specific balances, rates, income, and credit profile — and now you have the framework to figure that out without being taken advantage of.

About the Author

Written by Varn Kutser

Personal finance writer focused on savings, budgeting, and building wealth at Fabelo.io. Cuts through the noise to find accounts that actually earn.

Disclaimer: Rates and terms mentioned in this article are subject to change. Verify current rates directly with financial institutions before opening any account.

Last updated: April 12, 2026 · fabelo.io