Frugal Living Tips: The Complete Guide

The best frugal living tips cover food, spending, and daily habits. This complete guide covers beginner basics to extreme strategies that build lasting sav

Most people think frugal living means giving things up. It doesn't. The people who are genuinely good at spending less aren't depriving themselves — they've just stopped paying a premium for convenience they don't actually need. There's a real difference between being cheap and being intentional with money, and that distinction is what this guide is about.

Whether you're just starting out and looking for 50 frugal living tips for beginners, trying to build serious momentum with extreme frugal living tips, or simply want a handful of daily frugal living tips you can apply this week — this guide covers all of it. The strategies here range from Depression-era wisdom that has held up for nearly a century, to practical moves that make sense in a world where a Chipotle bowl costs $16 and streaming bundles quietly drain $80 a month from your checking account.

Start with the mindset shift: frugality is a skill, not a personality trait. You build it. And once you do, it gets easier every month.

Contents

- Frugal Living Tips from the Great Depression

- Frugal Living Tips for Beginners

- Daily Frugal Living Tips That Add Up Fast

- Extreme Frugal Living Tips

- Frugal Living at Every Life Stage

- Things No Longer Worth Buying

- Frugal Living Tips: Effort vs. Savings Comparison

- Watch This First

- What Real People Are Saying

- Frequently Asked Questions

- Your Next Steps

Frugal Living Tips from the Great Depression

The people who lived through the Great Depression didn't have the luxury of being sloppy with money. They developed habits that today's frugality community keeps rediscovering and calling "life hacks." These aren't nostalgic curiosities — they're durable strategies that still cut real costs in 2026.

Cook everything from scratch. This is the single highest-leverage food habit. Pre-packaged and processed foods carry a massive convenience markup. A loaf of artisan bread at a grocery store runs $5–$7. Made at home, the ingredient cost is closer to $1. Mayonnaise, salad dressings, soups, sauces — the same math applies across the board. According to Melissa K. Norris's frugal living research, cooking and preserving food at home was the cornerstone of Depression-era households — and the habits that people adopted out of necessity turned out to be some of the most effective money habits ever documented.

Eat at home, always. Eating out was a special occasion during the Depression, not a Tuesday. That framing makes sense financially. A family of four eating out even at a mid-range restaurant spends $60–$100 per meal. That same money, spent on groceries, feeds the family for several days.

Grow food if you can. Depression-era families planted every patch of available land. A small vegetable garden — even a few raised beds or container plants on a balcony — can produce hundreds of dollars of produce over a growing season. Tomatoes, leafy greens, herbs, and peppers are all high-yield options for small spaces. Frugal tips from that era also include growing fruit trees and foraging — both free food sources that take low effort once established.

Eat less meat. Meat was expensive in the 1930s and it's expensive now. Families stretched their protein budget with beans, eggs, lentils, and small amounts of cheaper cuts. Chicken legs and thighs instead of breasts. Canned tuna instead of fresh fish. This habit alone can reduce a grocery bill by 20–30% without any nutritional sacrifice.

Reuse and repurpose everything. Worn clothes got mended, not replaced. Glass jars became storage containers. Leftover food became tomorrow's soup. The Depression-era mindset — "use it up, wear it out, make it do, or do without" — is a practical operating principle that still holds up. Every item you repair instead of replace is money that stays in your pocket.

Make your own specialty coffee. A $6 daily coffee habit costs over $2,000 a year. Depression-era frugality would have called that absurd. A quality bag of whole beans, ground at home and brewed in a French press or drip machine, delivers a dramatically better cup for a fraction of the price. The habit isn't about deprivation — it's about not paying a 500% markup for something you can do yourself in five minutes.

Pack your lunch. Every single workday. This habit is worth $100–$200 a month for most people and it's the easiest daily frugal living habit to build once you get the routine down. Prep on Sundays, use leftovers strategically, and the savings compound fast.

Build a community and share resources. Depression-era neighborhoods shared. Neighbors split bulk purchases, traded skills, and helped each other through hard patches. Historical accounts of Depression-era frugality consistently point to community as a survival mechanism — borrowing tools, splitting large purchases, and bartering services. Splitting a Costco membership with a neighbor, or buying a bulk bag of rice with a friend, is the same strategy in modern form.

Frugal Living Tips for Beginners

Savings estimates in this guide are based on national averages, community-reported figures from Reddit, and published household spending data. Actual savings vary by location, household size, and spending habits.

If you're new to intentional spending, the best move is not to overhaul everything at once. Pick three habits, run them for 30 days, and build from there. Here are the most impactful starting points — these are the frugal living tips for beginners that give the fastest results with the lowest friction.

1. Build a real budget. Not a vague mental estimate — an actual written budget where every dollar has a category. Most people who start tracking their spending are shocked by what they find. Subscription services they forgot about. Food delivery totals that dwarf their grocery bill. A budget isn't a restriction; it's information. Once you have it, you can make real decisions.

2. Do a spending freeze. Pick one category — clothing, restaurants, entertainment — and freeze spending in it for 30 days. This does two things: it builds the muscle of intentional spending, and it reveals how much of your spending was habitual rather than needed. Most people who try a spending freeze discover they don't miss the category nearly as much as they expected.

3. Sell what you don't use. Go through your home methodically. Electronics, clothes, kitchen equipment, tools, sporting gear — anything sitting idle is cash waiting to be converted. Facebook Marketplace, eBay, and local buy-nothing groups make this easier than it's ever been. A single afternoon of decluttering can generate $200–$500 in cash and clear mental space in the process.

4. Stop buying things you don't need before you need them. This sounds obvious but it's one of the most common money leaks. Sales, bulk deals, and "just in case" purchases accumulate into clutter and wasted money. Buy what you need when you need it. If something is genuinely on sale and you'll use it — fine. But the "maybe someday" purchase is almost always a loss.

5. Audit every subscription. Streaming services, gym memberships, app subscriptions, SiriusXM, meal kit services — go through your bank and credit card statements line by line. Cancel anything you haven't actively used in the past 30 days. Most households carry $50–$150 in forgotten subscriptions. Canceling them is the closest thing to found money that exists.

6. Use the library aggressively. Books, audiobooks, e-books, magazines, DVDs, streaming through Libby and Kanopy — public libraries offer an enormous amount of entertainment and education for free. A library card is one of the most underused frugal tools available to Americans.

7. Automate savings before you can spend it. Set up an automatic transfer to a savings account the day after your paycheck arrives. Even $50 a paycheck adds up. The psychological effect of never seeing the money in your checking account makes saving dramatically easier than trying to save "whatever's left over" — because whatever's left over is usually nothing.

8. Compare prices before every significant purchase. Use browser extensions like Honey or Capital One Shopping to auto-apply coupons. Check CamelCamelCamel before buying anything on Amazon to see historical pricing. Never buy electronics, appliances, or furniture at full price when a 30-second price check might save you $50 or more.

Daily Frugal Living Tips That Add Up Fast

The big financial wins — buying a cheaper car, refinancing a mortgage, negotiating a salary increase — matter enormously. But the daily habits are what actually change your financial life, because they compound every single day. Here are the daily frugal living tips worth building into your routine.

Track what you spend every day. Even spending 60 seconds at the end of each day logging your purchases creates awareness that prevents mindless spending. Awareness is the first line of defense. Apps like YNAB, Copilot, or even a simple Notes file work.

Drink water. Skip the sodas, juices, and specialty drinks at restaurants and on the go. It sounds small, but a family of four ordering drinks at a restaurant adds $12–$20 to every bill. Over a month, that's real money. Water is free, and it's better for you.

Plan meals before grocery shopping. Shopping without a plan is the fastest way to waste food. You buy things you don't need, forget things you do, and end up with fridge waste. Plan the week's meals, write the list, stick to it. The USDA estimates American households throw away close to a third of the food they buy — meal planning directly attacks that waste.

Keep food expiration dates in mind. Rotate your fridge and pantry actively. Put items nearing expiration at the front. Use fruit that's about to turn before reaching for shelf-stable items. This is basic but most households don't do it consistently, and the cumulative waste is significant.

Bring a water bottle and travel mug everywhere. Buying a $3 water at the airport or a $5 coffee on the road is a habit tax. A good insulated mug pays for itself within a week. Keep a small cooler in your car with drinks if you're frequently on the road — it eliminates the gas station convenience store markup entirely.

Wait 48 hours before non-essential online purchases. Add items to your cart, then close the browser. Revisit in two days. A surprising number of "must-have" purchases look far less appealing after the initial impulse passes. This single habit can prevent hundreds of dollars in regretted spending each month.

Use what you have before buying more. Pantry, medicine cabinet, cleaning supplies, toiletries — most households have months of supplies buried somewhere. Run an inventory before restocking. This "use it up" mindset was central to Depression-era frugality and remains one of the most effective daily habits you can build.

Extreme Frugal Living Tips

Extreme frugal living is a legitimate strategy — particularly for people trying to eliminate debt aggressively, build an emergency fund fast, or accelerate toward a major financial goal. These tactics aren't for everyone, and they're not meant to be permanent for most people. But if you're serious about redirecting serious money in a short period of time, these are the levers that actually move the needle.

Move to a lower cost-of-living area. Housing is the largest expense in most American budgets. A person paying $2,500/month for a one-bedroom in a high-cost city who relocates to a mid-tier city and pays $1,100/month saves $16,800 a year — before touching any other expense. This is the single highest-impact financial move available to people who have location flexibility. It's disruptive, but the math is stark. Historical accounts note that during the Depression, families were willing to relocate entirely in pursuit of better economic conditions — and that willingness to move remains one of the most powerful financial tools available.

Eliminate the car payment. Drive whatever paid-off car you currently have as long as mechanically possible. Or sell a financed car, buy a reliable used vehicle for cash, and eliminate the monthly payment plus the insurance premium difference. The average new car payment in America is now above $700/month. That's $8,400 a year that could be doing something else.

House hack. If you own a home or rent a large enough unit, rent out a room or a basement apartment. Many people cover their entire mortgage or rent payment this way. It requires tolerance for shared space, but it effectively makes your housing cost zero or near zero — the most extreme version of housing expense reduction short of moving.

Go no-spend for an entire month. Commit to spending only on genuine necessities — groceries, utilities, transportation to work — for 30 full days. No restaurants, no entertainment spending, no clothing, no convenience purchases. People who do this consistently report saving two to three times what they expected, and they break habitual spending patterns that take months to rebuild.

Make your own cleaning products. White vinegar, baking soda, castile soap, and water handle the vast majority of household cleaning tasks. The ingredient cost is a fraction of branded cleaning products, the results are comparable, and you stop paying for packaging and marketing. This is a Depression-era habit that also eliminates dozens of synthetic chemicals from your home.

Cut your own hair, or extend cuts dramatically. Professional haircuts for a family of four add up to hundreds of dollars a year. Learning to do basic cuts at home — or extending the time between professional cuts from four weeks to eight — cuts this cost significantly. Men's clippers pay for themselves within two cuts.

DIY repairs before calling a professional. YouTube has made a remarkable range of home and car repairs accessible to anyone willing to spend an hour watching tutorials. Replacing a toilet flapper, patching drywall, changing brake pads, unclogging a drain — these repairs cost $10–$50 in parts and $150–$400 if you call someone. The skill pays dividends for life.

Negotiate every recurring bill. Internet, cell phone, insurance, gym memberships — these are all negotiable, especially if you're a long-term customer. Call, mention a competitor's rate, and ask for a retention discount. This works more often than most people expect. The effort is 20 minutes; the payoff can be $300–$600 a year in recurring savings.

Frugal Living at Every Life Stage

Frugal living looks different at 25 versus 45 versus 65. The principles are the same, but the priorities and tactics shift.

In your 20s and early 30s: This is the highest-leverage time to build frugal habits because your spending patterns are still forming and the compound interest on saved money is enormous over a 40-year horizon. Prioritize: avoiding lifestyle inflation as income grows, keeping fixed expenses low (housing and transportation especially), and building an emergency fund before anything else. If you can live on 60–70% of your income in your 20s, you're setting up a financial life that will be dramatically easier in every decade that follows.

In your 40s and 50s: Housing, kids, and career are typically the dominant financial forces. Frugality at this stage means resisting the pressure to upgrade everything — the house, the car, the vacation — as income rises. The trap is lifestyle inflation: earning more but saving the same percentage because expenses scaled with income. Reverse this by treating every raise as a savings increase first.

Frugal living at 60 and beyond: Fixed income or near-fixed income makes frugality less optional and more structural. Key moves: downsize housing if carrying a large home on a retirement budget, audit every insurance policy annually (rates shift considerably in this range), maximize Medicare supplement coverage to avoid catastrophic out-of-pocket health costs, and leverage senior discounts aggressively. Many restaurants, theaters, pharmacies, and retailers offer 10–20% senior discounts that go unused simply because people don't ask.

Travel on off-season schedules. In r/Fire, users consistently recommend traveling during shoulder season, staying at locally owned properties instead of chains, and eating where locals eat rather than at tourist-trap restaurants — all tactics that reduce travel costs by 30–50% without reducing the quality of the experience.

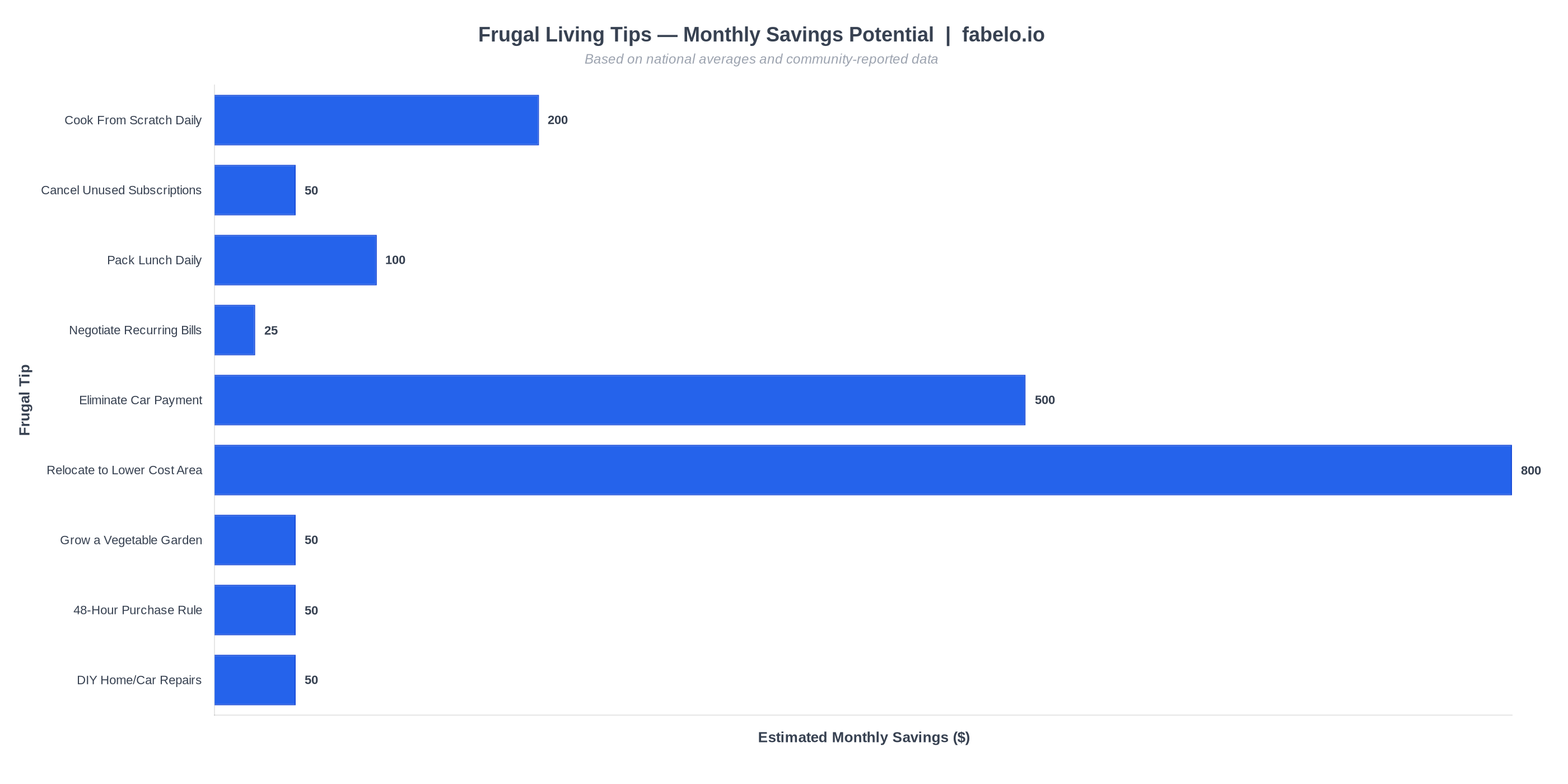

| Tip | Effort Level | Estimated Monthly Savings | Best For |

|---|---|---|---|

| Cook from scratch daily | Medium | $200–$400 | All levels |

| Cancel unused subscriptions | Low (one-time) | $50–$150 | Beginners |

| Pack lunch daily | Low–Medium | $100–$200 | All levels |

| Negotiate recurring bills | Low (one-time) | $25–$75 | All levels |

| Eliminate car payment | High (one-time) | $500–$800 | Extreme frugal |

| Relocate to lower cost area | Very High (one-time) | $800–$2,000+ | Extreme frugal |

| Grow a vegetable garden | Medium | $50–$150 | Homeowners/renters with outdoor space |

| 48-hour purchase rule | Low | $50–$300 | Impulse spenders |

| DIY home/car repairs | Medium–High | $50–$400 (variable) | Homeowners, car owners |

Things No Longer Worth Buying

The frugal living landscape in 2026 has a few specific landmines that deserve explicit attention — categories where costs have risen sharply while value has stayed flat or declined.

Fast and fast-casual food. This was once a budget option. It isn't anymore. A fast-casual meal for one person regularly clears $15–$18 with tax and tip. The value proposition has collapsed entirely. The Nicholas Garofola YouTube channel on frugal living noted exactly this shift: fast food used to justify itself on price and convenience, but the price has risen to the point where cooking at home is both cheaper and often more satisfying. Many people report that switching away from fast food also improved how they felt physically — a second benefit on top of the savings.

Streaming bundles and duplicate services. A single streaming service is a reasonable leisure expense. Four streaming services plus bundled add-ons is a different situation entirely. Bundle pricing is deliberately designed to make the math look appealing while obscuring how much you're actually spending. One service at a time, evaluated monthly, is the frugal approach — not a permanent bundle commitment that auto-renews indefinitely.

New technology at launch price. Phones, laptops, tablets, and gaming devices depreciate rapidly and often receive massive discounts within six to twelve months of launch. Paying $1,200 for a phone in September versus buying the same phone refurbished in March of the following year for $650 is a $550 difference for an identical device. There is almost never a functional justification for buying new tech at launch price.

Curbside grocery pickup. Many grocery chains charge a fee for curbside service, and shopping without walking the store can also mean missing markdowns and clearance items. Walking the store yourself — with a list — is nearly always cheaper.

Pre-packaged and processed meals. The markup on packaged convenience foods is substantial. A frozen meal for two might cost $9–$12. The same meal made from scratch costs $3–$5 in ingredients. The habit of cooking instead of buying packaged food is one of the clearest paths to consistent grocery savings.

Frugal Living Tips: Effort vs. Savings Comparison

Watch This First

Before you start building your frugal habits, this video offers a grounded perspective on where your money is actually going in 2026: Watch: Nicholas Garofola on frugal living and things no longer worth buying →

The core argument from the Nicholas Garofola YouTube channel is one worth sitting with: fast and fast-casual food has lost its value proposition entirely. What used to be a cheap, convenient option now regularly costs $15–$16 per person — and the experience rarely justifies it. The channel's perspective is that these rising prices have actually been a nudge toward better habits, particularly around cooking and baking at home. It's a reframe worth adopting: every price increase in a category you can replicate yourself is an invitation to build a skill and cut a cost simultaneously.

The channel also makes a sharp point about digital products and new technology: there is almost never a compelling reason to buy either at launch price. Games, apps, phones, and laptops all go on sale — often deeply — within months. Waiting is a strategy, not a sacrifice. If you can run your current phone for another year and skip the $1,200 upgrade cycle, you're not missing out. You're making a financially rational decision that most people around you aren't making.

What Real People Are Saying

The frugal living community online is active, opinionated, and often more practical than anything you'll find in mainstream personal finance coverage. The people on these forums are actually doing this, and their insights are sharper for it.

In r/Frugal, users consistently flag pre-packaged meals as one of the biggest money drains that people don't think about. One frequently upvoted perspective: you can make almost any packaged or prepared food yourself for a fraction of the cost — and once you develop the habit, the packaged version starts tasting worse by comparison. The same thread warns against curbside grocery pickup fees, which can quietly add $10–$30 per month without people noticing.

In r/Frugal, the most practical tip that surfaces repeatedly is food expiration management — keeping track of what's about to turn and eating it first, before touching shelf-stable items. It sounds basic. Most households don't actually do it. Reducing food waste by even 20% can trim a meaningful amount from the monthly grocery bill without buying anything differently.

In r/Fire, the travel advice is consistently smart: vacation during shoulder season, stay at locally owned spots instead of chain hotels, and eat at local restaurants instead of tourist-area markup traps. Users in that community report cutting travel costs by 40–50% just by shifting timing and accommodation choices — without any reduction in the quality or enjoyment of the trip.

And in r/Frugal discussions focused on food specifically, the protein rotation advice is a staple: chicken legs and thighs over breasts, eggs, beans, lentils, and rice as budget protein anchors. These aren't hardship foods — they're what the most cost-efficient home cooks in the world have used for generations. The nutrition is excellent; the cost is a fraction of packaged convenience proteins.

Frequently Asked Questions

What are the easiest frugal living tips for complete beginners?

Start with three habits that cost nothing to implement: build a written budget, pack your lunch every workday, and audit your subscriptions to cancel anything you haven't used in 30 days. These three moves alone can free up $200–$400 a month for most people. Once those are automatic, layer in meal planning and scratch cooking.

How much money can frugal living realistically save each month?

It depends entirely on your starting point and which habits you adopt. Beginners who tackle food spending and subscriptions typically save $200–$400 per month. People who implement extreme measures — eliminating a car payment, negotiating housing costs down, or doing a full spending freeze — can redirect $1,000 or more per month. The habits compound: each one makes the next one easier.

Is extreme frugal living sustainable long-term?

Extreme frugality is best used as a sprint, not a permanent lifestyle for most people. Use it to eliminate debt, build an emergency fund, or hit a specific savings goal — then pull back to a moderate frugal lifestyle once the goal is reached. Permanent extreme restriction tends to produce spending rebounds. Sustainable frugality is about reducing waste and intentional spending, not permanent deprivation.

What are the best frugal living tips specifically for food?

Cook from scratch whenever possible. Plan your meals before shopping. Buy chicken legs/thighs instead of breasts, and use beans, eggs, and lentils as primary protein sources. Never shop hungry. Rotate your fridge to use items near expiration first. Freeze anything you won't use before it turns. These habits combined can cut a typical family's food budget by 25–40%.

How do Depression-era frugal tips apply to modern life?

More directly than most people expect. The core Depression-era strategies — cook from scratch, grow what you can, repair before replacing, waste nothing, and build community resource-sharing — all map cleanly onto modern life. The specific tools are different (you're not darning socks by candlelight), but the principle of making do with less, extracting full value from everything you own, and avoiding convenience markups is identical. Depression-era frugal living strategies have proven remarkably durable because the underlying economics haven't changed: the more you can produce yourself, the less you have to buy.

What's the difference between being frugal and being cheap?

Frugal means maximizing value — spending deliberately and getting full use from what you buy. Cheap means minimizing cost at the expense of quality, relationships, or long-term value. A frugal person buys quality tools once and uses them for decades. A cheap person buys the lowest-price version repeatedly. Frugality is a long-term strategy; cheapness often costs more in the end.

Are there frugal living tips that don't require giving up things you enjoy?

Absolutely. The most sustainable frugal habits are about substitution and timing, not elimination. Make the coffee you enjoy at home instead of buying it out. Cook the restaurant meals you love in your own kitchen. Travel during shoulder season to the same destinations for dramatically less. Buy the electronics you want six months after launch at a significant discount. The experience is the same or better; the cost is lower.

Your Next Steps

Frugal living isn't a single decision — it's a collection of small habits that compound into a fundamentally different financial life over time. The people who are genuinely good at it didn't overhaul everything in a weekend. They built one habit, made it automatic, and added the next.

- This week: Audit every subscription and recurring charge on your bank and credit card statements. Cancel anything unused. This is a 45-minute task that pays you every month for the rest of the year.

- This month: Build a meal plan and cook every dinner at home for 30 days. Pack your lunch. Make your own coffee. Track what you spend daily. Calculate what you saved at the end of the month — that number will motivate the next phase.

- This quarter: Pick one bigger lever — negotiate your internet or cell phone bill, eliminate a car payment, learn one DIY repair skill, or start a container garden. These one-time actions create ongoing savings that require no daily effort to maintain.

The Depression-era frugalists didn't have a choice about living lean. You do — and that makes it a competitive advantage. Every dollar you redirect from waste into savings or investment is a dollar working for your future instead of someone else's bottom line.

About the Author

Written by Varn Kutser

Personal finance writer focused on savings, budgeting, and building wealth at Fabelo.io. Cuts through the noise to find accounts that actually earn.

Disclaimer: Rates and terms mentioned in this article are subject to change. Verify current rates directly with financial institutions before opening any account.

Last updated: April 12, 2026 · fabelo.io