High Yield Savings Account Rates: The Complete Guide

High yield savings account rates now reach 4%+ APY vs. the national average of 0.59%. Compare top banks, use the compound interest formula, and see real do

High yield savings account rates currently range from 3.50% to 4.00%+ APY � roughly 7 to 10 times the national average of 0.59%. On a $10,000 balance, that difference translates to $400 versus $59 per year. FDIC-insured, zero market risk, and you can open one online in under ten minutes.

All rates and APYs mentioned in this article are for illustration purposes. Rates change frequently � always verify current rates directly with your financial institution before making decisions.

The gap between a standard savings account and a high-yield one is not marginal � it's the difference between your emergency fund actively working for you and slowly losing ground to inflation. This guide covers the compound interest formula, a step-by-step calculation walkthrough, a comparison of the top high-yield savings account banks, and the exact questions real savers are asking right now.

Contents

- What High Yield Savings Account Rates Actually Mean

- The Compound Interest Formula for High Yield Savings

- Step-by-Step Worked Example Using a High Yield Savings Account Calculator

- Best High Yield Savings Account Banks Compared

- How to Read a High Yield Savings Account Comparison Before You Open One

- High Yield Savings Account Comparison at a Glance

- Watch This First

- What Real People Are Saying

- Frequently Asked Questions

- Your Next Steps

What High Yield Savings Account Rates Actually Mean

APY stands for Annual Percentage Yield. It reflects the true annual return on your savings, including the effect of compounding � meaning interest earned on interest already credited to your account. A 4.00% APY (rates change frequently � verify before opening) does not mean your balance grows by exactly 4% in one shot at year-end. It means interest compounds throughout the year (daily, monthly, or quarterly depending on the bank), and the cumulative effect equals 4.00% annually.

APR � Annual Percentage Rate � is different. APR is the simple interest rate without compounding. Banks quote APY on savings products because it's the more accurate and favorable-sounding number. When comparing accounts, always compare APY to APY, never APY to APR.

The national average savings rate sits at 0.59% APY (rates change frequently � verify before opening). Most traditional brick-and-mortar banks pay 0.01% to 0.10% on standard savings � essentially nothing. High-yield savings accounts, almost all of which are offered by online-only banks, pass along their lower overhead costs as higher interest to depositors. That structural advantage is why the rate gap is so wide and why it's likely to persist.

One thing savers frequently overlook: promotional vs. Permanent rates. Some banks advertise an elevated introductory APY (valid for 3�12 months for new customers) that drops to a lower base rate afterward. Others offer a consistently competitive ongoing rate. The difference matters enormously if you're parking a large emergency fund for years, not months. Always check whether the rate you're seeing is a promotional offer or the standard ongoing APY before opening an account. For a deeper look at how these accounts actually work, see our guide on high yield savings accounts.

Compounding frequency also matters, though the difference is modest at consumer savings rates. Daily compounding (365 periods/year) produces slightly more than monthly compounding (12 periods/year). At 4.00% APY (rates change frequently � verify before opening), the stated APY already accounts for the compounding schedule, so comparing APY figures directly is still valid. But if you ever see a bank quoting only APR, use the formula below to convert it to APY yourself.

The Compound Interest Formula for High Yield Savings

The math behind high yield savings account rates is straightforward once you see it clearly. There are two formulas worth knowing: one for a lump-sum deposit, and one that adds regular monthly contributions.

Formula 1: Lump-Sum Deposit

A = P � (1 + r/n)^(n�t)

- A = Final balance (what you end up with)

- P = Principal (initial deposit)

- r = Annual interest rate as a decimal (e.g., 4.00% = 0.04)

- n = Compounding periods per year (12 = monthly, 365 = daily)

- t = Time in years

If your bank compounds daily, use n = 365. If monthly, use n = 12. Most high-yield savings accounts compound daily, which is why you'll often see online savings calculators default to daily compounding.

Formula 2: With Regular Monthly Contributions

This formula adds a recurring monthly deposit (PMT) on top of the initial principal:

A = P � (1 + r/n)^(n�t) + PMT � [((1 + r/n)^(n�t) ? 1) / (r/n)]

- PMT = Monthly contribution amount

- All other variables are the same as above

This second formula is what SoFi's savings account calculator and Marcus by Goldman Sachs's high-yield savings calculator use under the hood. Understanding the formula lets you stress-test any scenario without depending on a specific tool � and it helps you understand exactly why small rate differences compound into significant dollar gaps over multi-year timeframes.

To understand how this compounding mechanic scales over longer investment horizons, the compound interest formula guide walks through the math in full detail, including edge cases and conversion between APR and APY.

Step-by-Step Worked Example Using a High Yield Savings Account Calculator

Real numbers make this concrete. Here's a full walkthrough using a realistic scenario: someone with $15,000 in initial savings, adding $300/month, at a 3.75% APY (rates change frequently � verify before opening) compounded daily over 3 years.

Given values:

- P = $15,000

- PMT = $300/month

- r = 3.75% = 0.0375

- n = 365 (daily compounding)

- t = 3 years

Step 1: Calculate the growth of the initial principal.

A? = 15,000 � (1 + 0.0375/365)^(365�3)

= 15,000 � (1.000102739...)^(1095)

? 15,000 � 1.11881

? $16,782.15

Step 2: Calculate the future value of the monthly contributions.

For monthly contributions with daily compounding, convert to monthly rate: monthly rate ? 0.0375/12 = 0.003125

A? = 300 � [((1.003125)^36 ? 1) / 0.003125]

= 300 � [(1.11934 ? 1) / 0.003125]

= 300 � [0.11934 / 0.003125]

= 300 � 38.189

? $11,456.70

Step 3: Add them together.

Total balance = $16,782.15 + $11,456.70 = $28,238.85

Step 4: Calculate total interest earned.

Total deposited = $15,000 + ($300 � 36 months) = $15,000 + $10,800 = $25,800

Interest earned = $28,238.85 ? $25,800 = $2,438.85

Now compare that to the same $25,800 total deposited at the national average rate of 0.59%:

The difference between a top-tier HYSA and a typical big bank over just three years: $2,434.98 in extra interest. That's real money � a car repair, a month's rent, or a meaningful head start on an IRA contribution. The First City Credit Union interest calculator and Bell Bank's HYSA calculator are two free tools you can use to run your own numbers with different contribution amounts and timeframes.

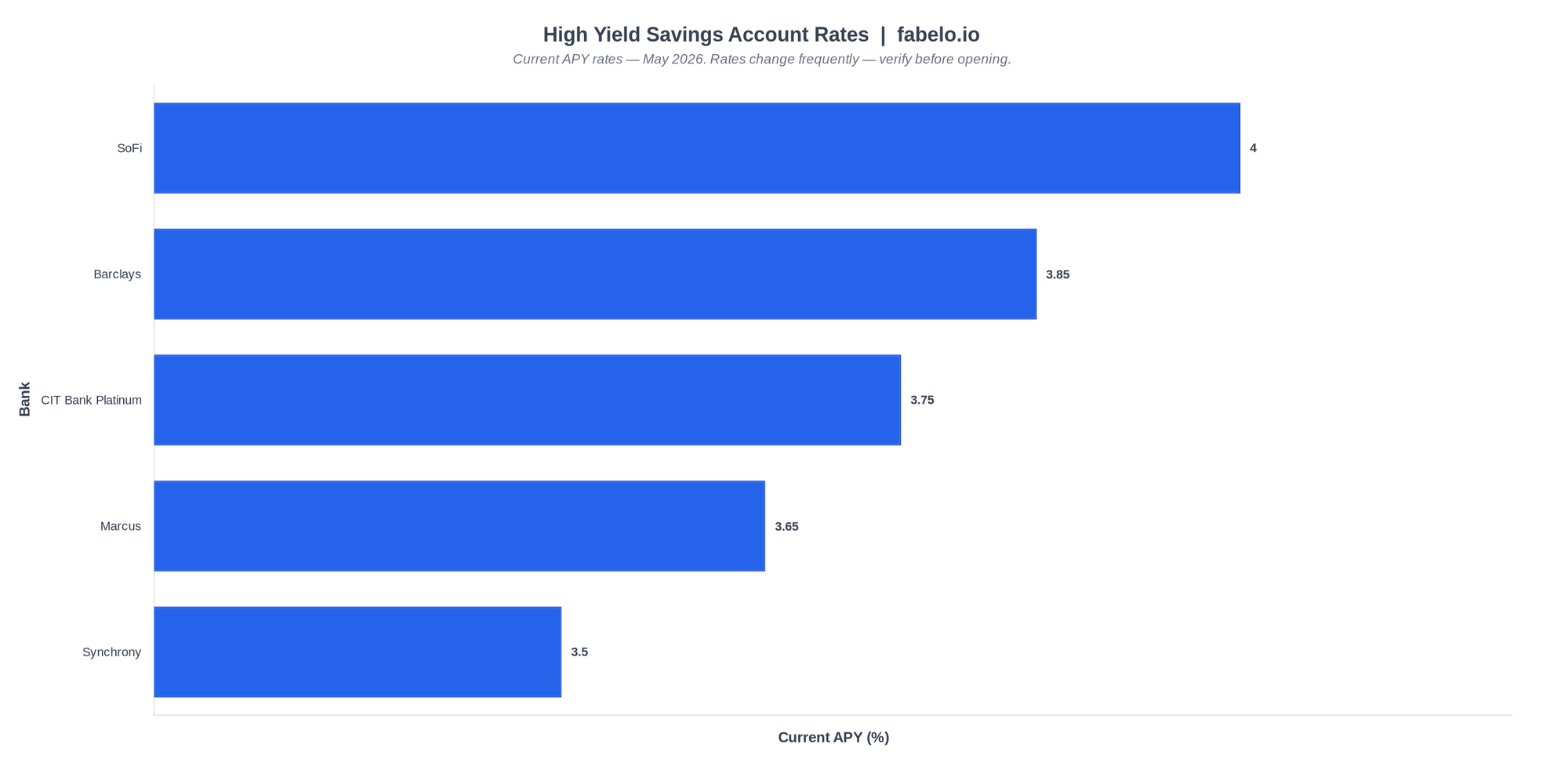

Best High Yield Savings Account Banks Compared

Here are the top accounts worth considering right now. Rates shift constantly, so treat every figure below as a current snapshot � always confirm directly with the bank before opening.

Savings estimates and rate comparisons in this section are based on national averages, community-reported figures, and published institutional data. Actual earnings vary by balance, timing, and account eligibility.

SoFi Bank

Current APY: Up to 4.00% (PROMOTIONAL � requires eligible direct deposit; base rate is 3.30%)

Minimum opening deposit: $0

Monthly fees: $0

FDIC insurance: Standard $250,000 per depositor

Unique feature: Full-platform banking � checking, investing, loans, and crypto all in one app

SoFi's top rate requires setting up a qualifying direct deposit � without it, the rate drops to 1.00% APY (rates change frequently � verify before opening). The 0.70% APY (rates change frequently � verify before opening) boost on top of the 3.30% base is promotional and subject to change. For savers willing to route their paycheck through the account, it's one of the most competitive all-in-one banking options available. The $0 minimum and no monthly fees lower the barrier to entry significantly. According to the Watch: the NerdWallet YouTube channel on best high-yield savings account rates of 2026 🎬 video on the Charlie Chang YouTube channel, SoFi also offers cash bonuses � $50 with $1,000 in direct deposits and $300 with $5,000 or more � though bonus availability should be verified at time of opening.

Best for: Savers who want a single banking app and are comfortable routing their paycheck through an online bank.

Barclays Online Savings

Current APY: 3.70% (balances under $250,000); 3.85% (balances of $250,000+) � PERMANENT rates, no direct deposit required

Minimum opening deposit: $0

Monthly fees: $0

FDIC insurance: Standard $250,000 per depositor

Unique feature: Tiered rate structure � larger balances automatically earn a higher APY with no action required

Barclays is one of the largest financial institutions in the world, and its online savings product strips away all the complexity. No minimum balance, no monthly fee, and a solid ongoing rate that doesn't depend on any qualifying activity. The tiered structure rewards savers with larger balances without requiring separate account types. There's no mobile check deposit or ATM access � it's purely a savings vehicle � but for savers who just want a reliable, no-hassle rate, Barclays delivers.

Best for: Savers who want a consistent rate without jumping through qualification hoops, especially those holding balances above $50,000.

Synchrony Bank High Yield Savings

Current APY: 3.50% � PERMANENT

Minimum opening deposit: $0

Monthly fees: $0

FDIC insurance: Standard $250,000 per depositor

Unique feature: ATM card with access to 400,000+ fee-free ATMs nationwide and up to $5 out-of-network ATM fee reimbursement per statement cycle

Synchrony's defining feature in this category is its ATM card � virtually no other high-yield savings account at a comparable rate offers this. For savers who occasionally need cash access from their savings without a full transfer to checking first, Synchrony eliminates that friction. The account also allows unlimited withdrawals, which is more flexible than some competitors. The rate, at 3.50%, is slightly below the top tier but has remained consistently competitive through multiple Fed rate cycles. Reliability counts for something.

Best for: Savers who want occasional cash access from their savings account without maintaining a separate checking relationship.

CIT Bank Platinum Savings

Current APY: 3.75% for balances of $5,000+; drops to 0.25% below $5,000 � PERMANENT

Minimum opening deposit: $100

Monthly fees: $0

FDIC insurance: Standard $250,000 per depositor

Unique feature: No balance cap � the 3.75% rate applies equally whether you hold $5,000 or $2 million

CIT Bank's Platinum Savings account is powerful for savers who maintain a consistent balance above $5,000 � which should cover most people using a HYSA for an emergency fund or targeted savings goal. The rate drop to 0.25% below $5,000 is steep, so this account demands discipline. But for anyone who won't dip below that threshold, the 3.75% permanent rate with no balance ceiling is genuinely compelling. There's no concern about being penalized for growing your balance too large. The $100 minimum opening deposit is modest.

Best for: Disciplined savers who maintain balances consistently above $5,000 and don't want to worry about rate caps at higher balances.

Marcus by Goldman Sachs Online Savings

Current APY: Approximately 3.65% � includes a promotional rate boost for new accounts; verify current ongoing rate directly

Minimum opening deposit: $0

Monthly fees: $0

FDIC insurance: Standard $250,000 per depositor

Unique feature: Loyalty Rate program � Marcus may offer existing customers a rate boost if the standard rate decreases

Marcus has one of the cleaner account experiences in online banking � no minimum, no fees, and a consistently competitive rate backed by Goldman Sachs's institutional stability. The Goldman Sachs name carries regulatory and capital weight that some newer fintech banks can't match, which matters for savers depositing larger amounts. Marcus also offers a high-yield savings calculator that lets you directly compare your potential earnings against national averages � a genuinely useful planning tool.

Best for: Savers who prioritize institutional stability and want a no-friction account backed by a name-brand financial institution.

Ally Bank Online Savings

Current APY: Verify on their site � historically 3.60%�4.00% range; rates adjust with Fed movements

Minimum opening deposit: $0

Monthly fees: $0

FDIC insurance: Standard $250,000 per depositor

Unique feature: Savings "buckets" � virtual sub-accounts within a single savings account for goal-based saving

Ally has been one of the most recognizable names in online high-yield savings for over a decade. The savings buckets feature lets you organize your money by goal � emergency fund, vacation, car repair � without opening multiple accounts. Ally's savings interest calculator is one of the cleaner tools for understanding how compounding works on your specific balance. The app experience is consistently rated among the best in the category. This is a strong choice for savers who want visual organization of their goals alongside a competitive rate.

Best for: Savers who want goal-based organization tools and a polished mobile banking experience.

How to Read a High Yield Savings Account Comparison Before You Open One

Most high-yield savings account comparison tools show APY and not much else. That's a problem, because the rate alone doesn't tell you the full story. Here's what to check before clicking "open account."

1. Promotional vs. Ongoing rate. A bank advertising 4.50% APY (rates change frequently � verify before opening) might be offering that rate only for the first 6 months or only to new customers. After the promo period, the rate could drop to 3.00% or lower. Always look for the "after promotional period" rate in the fine print. Tools like depositaccounts.com track rate histories so you can see how competitive a bank has been over time, not just today.

2. Rate requirements. Some accounts require direct deposit to earn the top rate (SoFi), while others require a minimum balance (CIT Bank's $5,000 threshold). If you can't or won't meet the requirement, the effective rate you'll earn is much lower. Calculate your real expected APY based on your actual situation.

3. Compounding frequency. Daily compounding beats monthly compounding, all else equal. At 4.00% APY (rates change frequently � verify before opening), this difference is negligible � a few dollars annually on a $10,000 balance. But the APY figure already incorporates compounding, so comparing APYs head-to-head is still valid regardless of compounding schedule.

4. FDIC or NCUA coverage. Every account in this guide carries standard FDIC insurance of $250,000 per depositor per institution. If you're holding more than $250,000 in savings, consider spreading across multiple institutions or look for banks offering enhanced coverage through deposit sweep programs. Some fintech platforms pass deposits through to multiple FDIC-member banks, effectively multiplying your insured limit. This is a niche situation for most people, but worth knowing.

5. Transfer speed. Some online banks take 2�5 business days to transfer funds to an external account. If your HYSA is also your emergency fund, a slow transfer can create real problems in an actual emergency. Check the bank's standard transfer timeline before committing. Same-day or next-day transfers are available at some banks but not all. If you're building your emergency fund and want to see the broader savings strategy, the guide on how to save money fast covers the account setup alongside the savings behaviors that accelerate progress.

6. Monthly fees. Every account in this comparison charges $0/month. If you encounter a HYSA that charges a monthly maintenance fee, the math almost never works in your favor. Even a $5/month fee on a $5,000 balance at 3.75% APY (rates change frequently � verify before opening) costs you $60/year against $187.50 in interest � wiping out nearly a third of your earnings.

\n

| Scenario | APY | Total Deposited | Final Balance (3 yrs) | Interest Earned |

|---|---|---|---|---|

| High-Yield (3.75% APY (rates change frequently � verify before opening)) | 3.75% | $25,800 | $28,238.85 | $2,438.85 |

| National Average (0.59% APY (rates change frequently � verify before opening)) | 0.59% | $25,800 | $26,260.42 | $460.42 |

| Typical Big Bank (0.01% APY (rates change frequently � verify before opening)) | 0.01% | $25,800 | $25,803.87 | $3.87 |

\n

High Yield Savings Account Comparison at a Glance

Use this table to compare the key terms across the accounts covered above. Confirm all figures directly with each institution before opening � rates and promotions change regularly.

\n

| Bank | Current APY | Rate Type | Min. Deposit | Monthly Fee | FDIC Limit | Standout Feature |

|---|---|---|---|---|---|---|

| SoFi | Up to 4.00% | Promotional (requires direct deposit) | $0 | $0 | $250,000 | All-in-one banking platform |

| Barclays | 3.70% / 3.85% | Permanent (tiered by balance) | $0 | $0 | $250,000 | Automatic tier upgrade at $250K |

| Synchrony | 3.50% | Permanent | $0 | $0 | $250,000 | ATM card, 400K+ fee-free ATMs |

| CIT Bank Platinum | 3.75% (?$5K) | Permanent (balance threshold) | $100 | $0 | $250,000 | No balance ceiling on top rate |

| Marcus | ~3.65% | Permanent + new account promo | $0 | $0 | $250,000 | Loyalty Rate protection program |

| Ally | Verify on site | Permanent | $0 | $0 | $250,000 | Savings "buckets" for goal tracking |

\n

Watch This First

Watch: the NerdWallet YouTube channel on best high-yield savings account rates of 2026 🎬

The Charlie Chang YouTube channel covers the top five high-yield savings accounts in detail, and a few points stand out. First, the channel emphasizes that SoFi's elevated rate is a promotional boost stacked on top of a base rate � a distinction that matters enormously for long-term savers who assume the headline rate is permanent. Without direct deposit setup, the rate drops dramatically, which is a practical detail many savers miss when opening an account based on an advertised headline APY.

A second insight worth highlighting: Synchrony's ATM card feature is flagged as genuinely rare in this category. Most HYSAs are designed to be locked away from easy access � that's partly how they stay funded at high rates. Synchrony's decision to offer ATM access is a deliberate design choice that trades some separation-from-savings discipline for real-world flexibility. Whether that trade-off helps or hurts you depends entirely on your own spending habits.

The channel also makes a point that applies across every account in this guide: rates shift constantly with Federal Reserve movements, and what's true when any video or article is published may be different by the time you watch or read it. The practical takeaway is to use any rate comparison as a directional shortlist, then verify current figures directly on each bank's site before opening. Depositaccounts.com is worth bookmarking for ongoing rate tracking.

What Real People Are Saying

In r/povertyfinance, users consistently push back on the idea that HYSAs are only for people with large balances. The most upvoted advice in recent threads: move your emergency fund out of a traditional bank regardless of how small it is. Even $500 earning 3.75% APY (rates change frequently � verify before opening) beats $500 earning 0.01% by a factor of 375. The math doesn't require a large balance to be worth it.

In r/HighYieldSavings, the conversation around "best rate right now" moves fast. Community members note that top rates fluctuate weekly and that smaller, less-known banks occasionally top the rate charts briefly before settling back. The consistent advice: track rates on aggregator sites rather than relying on any single article or video, since rates shift between Fed meetings and sometimes between weeks.

In r/TheMoneyGuy, users report watching their HYSA rates drift downward over 2024�2025, with one user noting their account dropped from an intro rate above 4% to a standard ongoing rate around 3.50%. This mirrors the broader rate environment as the Federal Reserve has cut the federal funds rate from its 2023�2024 highs. The lesson: intro rates are real money while they last, but planning around a permanent rate requires looking at the base, not the promotional headline. Users in r/personalfinance also flag Synchrony Bank positively for maintaining rate competitiveness through the current rate-declining cycle, which aligns with what the community data consistently shows about Synchrony's long-term reliability.

Frequently Asked Questions

Which bank gives 7% interest on a savings account in the United States?

No mainstream U.S. Bank currently offers 7% APY on a standard savings account. The 7�8% rates referenced in some searches are from small finance banks in India (like Suryoday Small Finance Bank or Equitas Small Finance Bank), not U.S. Institutions. In the U.S., top high-yield savings account rates currently range from 3.50% to 4.00%+ APY. Some credit unions run occasional promotional rates above 5% on limited-balance accounts, but these typically apply only to the first $500�$1,000. Always check that a rate you find is from an FDIC- or NCUA-insured U.S. Institution.

How much interest does $10,000 earn in a high-yield savings account over 12 months at 4.00% APY (rates change frequently � verify before opening)?

At 4.00% APY (rates change frequently � verify before opening) compounded daily, $10,000 earns approximately $408 over 12 months, bringing your balance to roughly $10,408. At the national average of 0.59% APY (rates change frequently � verify before opening), the same $10,000 earns about $59, ending at $10,059. The difference � $349 per year � compounds even further if you leave the interest in the account. At 3 years with no additional contributions, the HYSA balance reaches approximately $11,272 versus $10,178 at the national average.

Is it better to open a high-yield savings account or a money market account for emergency savings?

For most people with emergency funds under $250,000, a high-yield savings account is the better choice right now. Money market accounts at online banks offer similar or slightly lower rates, and many require higher minimum balances ($1,000�$2,500) to avoid fees or earn the top rate. The practical difference for an emergency fund is minimal � both are FDIC-insured, both are liquid, and both are better than a traditional savings account by a wide margin. If you need check-writing access to your savings, a money market may edge out an HYSA for convenience.

Do high-yield savings account rates move with the Federal Reserve, and what happens if rates drop?

Yes, HYSA rates track the federal funds rate closely � not on a fixed schedule, but directionally and within weeks of any Fed move. When the Fed raises rates, HYSA rates go up. When the Fed cuts rates, HYSA rates follow. This is exactly what happened in 2024 and into 2025: peak HYSA rates reached 5.00%+ APY in 2023, then drifted down as the Fed began cutting. Current rates in the 3.50%�4.00% range reflect that adjustment. If rates continue falling, HYSAs remain the best liquid cash option � they'll still beat money market mutual fund yields for most balances and remain far above traditional savings accounts.

Can I use a high-yield savings account calculator to estimate monthly interest earnings instead of annual?

Yes. To calculate monthly interest from a stated APY, use this approach: divide the APY by 12 for an approximation, then apply it to your current balance. On $20,000 at 3.75% APY (rates change frequently � verify before opening), monthly interest is approximately $20,000 � (0.0375 / 12) = $62.50 per month. Online calculators at SoFi and Marcus allow you to switch between monthly and annual views directly. For a deeper dive into how compounding amplifies these monthly figures over time, the compound interest calculator guide walks through the mechanics in detail.

What's the difference between a high-yield savings account and a CD for someone saving over a 2-year horizon?

A CD (Certificate of Deposit) locks your rate � and your money � for a fixed term. If you deposit into a 2-year CD at 4.00% APY (rates change frequently � verify before opening) today, that rate is guaranteed regardless of what the Fed does. A HYSA gives you flexibility but a variable rate � if the Fed cuts rates four more times over those two years, your HYSA yield could drop to 2.50% or lower. For money you won't need for exactly 2 years, a CD may produce better guaranteed returns in a declining rate environment. For true emergency funds you might need without notice, a HYSA's liquidity is non-negotiable. Many savers use both: a HYSA for 3�6 months of expenses, and a CD ladder for the rest of their cash reserves.

How does a high-yield savings account fit into a broader wealth-building plan, and when should I stop prioritizing it?

A HYSA earns 3.50%�4.00% APY (rates change frequently � verify before opening) � which is excellent for cash but trails long-term stock market returns (historically 7�10% annually over multi-decade periods). The right use of a HYSA is for money you need liquid and safe: emergency fund (3�6 months of expenses), near-term savings goals (car, home down payment within 1�3 years), or cash awaiting deployment into investments. Once your emergency fund is fully funded, additional savings are generally better directed toward tax-advantaged accounts � 401(k), IRA, or Roth IRA. If you're still building toward those goals, the guide on how to build wealth in your 20s covers exactly this sequencing.

Your Next Steps

The mechanics are clear. The math is compelling. Here's what to actually do next.

Step 1: Calculate your realistic earnings today. Take your current savings balance and multiply it by 0.0375 (for 3.75% APY (rates change frequently � verify before opening)) to get your approximate annual interest. If that number is significantly higher than what your current bank is paying, you have a concrete dollar reason to switch. Use the SoFi savings calculator or Marcus's HYSA calculator to model your specific numbers with monthly contributions included.

Step 2: Match the account to your situation. If you want zero qualification requirements and a consistent rate, Barclays or CIT Bank (if you maintain $5,000+) fit best. If you want everything in one app and will set up direct deposit, SoFi's rate is compelling. If you need occasional ATM access from savings, Synchrony is the only account in this comparison that gives you a card. There's no single "best" HYSA � the best one is the one whose rate requirements you'll actually meet.

Step 3: Set it and monitor it � not obsessively, but quarterly. Open the account, fund it, and schedule a quarterly 5-minute check to confirm the rate is still competitive. Depositaccounts.com and similar aggregators make this fast. If your bank drops its rate by 0.50% or more below the top market rate, it takes about 15 minutes to open a new account at a competitor. Inertia is the most expensive thing in personal finance � it costs savers hundreds of dollars per year at the national average rate when a competitive alternative is one form-fill away.

About the Author

Written by Varn Kutser

Personal finance writer covering savings, investing, and budgeting with a data-first approach. Every rate, limit, and claim is verified against official sources � FDIC, IRS, and Federal Reserve. No clickbait, no guesswork, just numbers.

Disclaimer: Rates and terms mentioned in this article are subject to change. Verify current rates directly with financial institutions before opening any account.

Last updated: April 29, 2026 � fabelo.io