Roth IRA Calculator: The Complete Guide

A Roth IRA calculator shows your tax-free retirement balance using your age, contributions, and expected return. See what $100/month grows to in 30 years.

A Roth IRA calculator estimates your tax-free retirement balance based on your current age, annual contributions, and an assumed rate of return. Contribute $100 a month starting at age 25, assume a 7% average annual return, and a Roth IRA growth calculator projects roughly $121,000 by age 55 — and closer to $243,000 by age 65. Every dollar grows tax-free and withdrawals in retirement cost you nothing in federal income tax.

The problem is that not all free Roth IRA calculators are built the same. Some are barebones — they give you a final number with no breakdown. Others let you model contribution increases over time, compare Roth vs. Traditional scenarios, or factor in your current tax bracket. This guide ranks the best options, explains exactly what each one does well, and tells you which calculator is worth your time based on where you are in your retirement planning.

All rates and return assumptions mentioned in this guide are for illustration purposes only. Rates and market returns change frequently — always verify assumptions with a qualified financial professional before making retirement decisions.

Contents

- Bankrate Roth IRA Calculator: Best for Beginners

- Calculator.net Roth IRA Calculator: Best for Detailed Projections

- NerdWallet Roth IRA Calculator: Best for Contribution Limits

- Fidelity Roth Conversion Calculator: Best for Conversion Decisions

- Charles Schwab Roth vs. Traditional IRA Calculator: Best for Tax Bracket Comparison

- Landmark Credit Union Roth IRA Calculator: Best for Credit Union Members

- Roth IRA Calculator by Age: What the Numbers Actually Look Like

- Quick Comparison of the Best Free Roth IRA Calculators

- Watch This First: Roth Conversions, Tax Strategy, and the Numbers That Matter

- What Real People Are Saying About Roth IRA Calculators

- How We Chose the Best Roth IRA Calculators

- Frequently Asked Questions About Roth IRA Calculators

- Final Verdict

Roth IRA Calculator: Best for Beginners

The Bankrate Roth IRA calculator is the most widely used free Roth IRA calculator in the U.S. For good reason — it loads fast, asks only the inputs that matter, and gives you a clean projection without overwhelming someone who's just getting started. Enter your current age, planned retirement age, current Roth IRA balance (even if it's $0), annual contribution amount, and an expected rate of return. The tool instantly calculates your projected balance at retirement.

What makes 's version particularly beginner-friendly is that it prefills a 6% return assumption and explains its methodology right on the page. If you're 30 years old, contributing $6,500 per year (the 2024 standard limit), and starting from zero, the calculator shows a projected balance of approximately $504,000 by age 65 — assuming 6% average annual growth. Bump the return assumption to 7% and that number climbs past $600,000. The tool makes these adjustments in real time, which helps new investors understand how powerfully return rate affects long-term outcomes.

The interface is clean enough for a first-time investor but detailed enough to be genuinely useful. You can toggle your contribution frequency between annual and monthly, which matters if you're trying to match how you actually budget. There's no login required, no account creation, and no upsell buried in the results — just the projection.

One limitation: Bankrate's calculator doesn't model income-based contribution phase-outs. If you're a high earner approaching the Roth IRA income limits (single filers: $146,000–$161,000 in 2024; married filing jointly: $230,000–$240,000), this calculator won't automatically flag that your contribution may be reduced. You'll need a separate tool for that. The calculator also doesn't compare Roth vs. Traditional IRA tax outcomes — it's strictly a Roth IRA growth calculator. For a full breakdown of how much you're legally allowed to contribute, check our guide on Roth IRA contribution limits.

Pros

- No login or account required

- Extremely fast, clean interface

- Allows monthly or annual contribution input

- Prefilled return assumption with explanation

- Trusted, well-maintained tool updated regularly

Cons

- Does not model income-based Roth IRA phase-outs

- No Roth vs. Traditional comparison feature

- No year-by-year balance breakdown table

- Single return rate assumption — no range modeling

Who It's For

Anyone opening their first Roth IRA or wanting a quick, no-nonsense projection. Ideal for people in their 20s and 30s who just want to see the end number and understand how contributions compound over decades.

Real-world scenario: A 28-year-old nurse earning $65,000/year wants to know what happens if she contributes $300/month starting today. 's calculator gives her the answer in under 30 seconds: approximately $875,000 at 65 assuming a 7% return. No spreadsheet needed. That's the value here.

Calculator.net Roth IRA Calculator: Best for Detailed Projections

The Calculator.net Roth IRA calculator goes significantly deeper than most free tools. It's not pretty — the interface is dense and utilitarian — but for anyone who wants to understand the year-by-year mechanics of Roth IRA compounding, it's the most thorough free option available without paying for financial planning software.

The standout feature is the annual schedule table. After you input your variables, the tool generates a complete year-by-year breakdown showing your beginning balance, annual contribution, earnings for that year, and cumulative total. This is the kind of transparency that helps you see exactly when your investment earnings start to outpace your contributions — typically somewhere between years 15 and 20 for most investors. Understanding that inflection point is genuinely motivating and helps people stick to consistent contributions.

Calculator.net's tool also handles tax savings comparisons. It shows the after-tax value of your Roth IRA versus what a taxable account would produce under the same return assumptions, illustrating the real dollar value of the tax-free growth benefit. For someone in the 22% federal bracket contributing for 30 years, that difference can easily be $100,000 or more in tax savings at withdrawal time.

You can input contributions in monthly or annual terms, set a custom annual return rate, and specify the number of years until retirement. The tool also lets you model an initial lump-sum deposit alongside ongoing contributions — useful if you've inherited money or received a bonus you're considering depositing into a Roth.

The weakness is the user experience. There's no visual chart, no mobile-optimized layout, and the dense table output can be confusing for people who aren't comfortable reading multi-column financial tables. If you're new to IRAs, start with . Once you're ready to understand the mechanics, come back to Calculator.net.

Pros

- Full year-by-year amortization schedule

- Compares Roth growth vs. Taxable account outcomes

- Handles lump-sum plus ongoing contribution modeling

- No login, completely free

- Most comprehensive free output of any tool on this list

Cons

- Dated, non-responsive interface

- No visual chart output

- Overwhelming for beginners

- No income phase-out modeling

Who It's For

Data-driven investors, spreadsheet users, and anyone who wants to see the exact year their Roth IRA balance hits a specific milestone. Also great for people comparing the value of Roth IRA tax-free growth against taxable brokerage accounts.

Roth IRA Calculator: Best for Contribution Limits

The NerdWallet Roth IRA calculator does something no other tool on this list does by default: it actively checks your income against current IRS contribution limits and tells you exactly how much you're eligible to contribute this year. For anyone earning above $130,000 as a single filer or approaching the married filing jointly phase-out range, this is critical information most calculators simply ignore.

The input flow is more conversational than most tools. You enter your filing status, modified adjusted gross income (MAGI), and age, and the calculator first confirms your eligibility and maximum contribution before projecting your retirement balance. If you're in the phase-out range, it calculates your reduced contribution limit to the dollar — a detail that matters if you're trying to avoid an IRS excess contribution penalty.

The growth projection itself uses a 6% default return with an adjustable slider, and the results include a clean bar chart showing year-by-year balance growth. It's visually accessible in a way Calculator.net isn't. Also embeds explanatory notes directly next to each input field, making the tool educational as you use it — not just after you get a result.

The unique feature here is contribution eligibility verification integrated into the calculator flow. No other free tool on this list automatically cross-references your income against the current year's phase-out thresholds before running the projection. That alone makes this the go-to tool for anyone whose income is anywhere near the Roth IRA eligibility ceiling.

The limitation is that the tool doesn't model Roth conversions or compare Roth vs. Traditional outcomes from a tax-bracket perspective. It's purely a contribution eligibility checker plus growth projector — two things it does extremely well.

Pros

- Built-in income eligibility and phase-out calculation

- Visual bar chart output

- Conversational, guided input flow

- Inline explanations for every input field

- Updated annually to reflect current IRS limits

Cons

- No Roth vs. Traditional comparison

- No Roth conversion modeling

- Requires more inputs than before showing results

Who It's For

Higher-income earners (roughly $120,000–$240,000/year) who need to confirm their eligibility before contributing. Also ideal for anyone who wants an accurate maximum contribution figure for the current tax year.

Fidelity Roth Conversion Calculator: Best for Conversion Decisions

Every other calculator on this list projects future Roth IRA growth from new contributions. The Fidelity Roth Conversion Calculator asks a fundamentally different question: should you move money from a traditional, rollover, SEP, or SIMPLE IRA into a Roth IRA right now, and what does the math actually look like?

Roth conversions are a legitimate strategy — especially for people in temporarily low-income years, those who've recently retired but haven't started Social Security yet, or anyone who expects to be in a higher tax bracket in the future. The mechanics are straightforward: you pay ordinary income tax on the converted amount today, then that money grows and is withdrawn completely tax-free. The question is always whether paying taxes now beats paying taxes later.

Fidelity's tool models this comparison directly. You input your current traditional IRA balance you want to convert, your current federal and state tax rates, your expected tax rate in retirement, and your investment time horizon. The calculator then runs both scenarios — convert now vs. Don't convert — and shows the after-tax account value at retirement under each approach. It accounts for the taxes you'd pay on the conversion today and models how much those converted funds compound over time versus the alternative.

The unique feature Fidelity's calculator has that no other tool on this list offers is the tax rate sensitivity analysis. It shows you at what future tax rate the conversion breaks even — meaning the threshold where converting becomes mathematically beneficial versus leaving funds in the traditional IRA. This kind of decision-support analysis is what financial planners charge hundreds of dollars to produce.

You'll need a Fidelity account to save your results, but the calculator itself runs without logging in. The interface is clean and the output is actionable. If you have a 401(k) or traditional IRA and you're even casually thinking about a Roth conversion, this tool gives you a concrete number to evaluate — not just a general recommendation.

Pros

- Purpose-built for Roth conversion analysis, not just contribution projections

- Models both federal and state tax impacts

- Break-even tax rate analysis included

- Handles traditional, SEP, SIMPLE, and rollover IRA conversions

- Free to use without an account

Cons

- Not useful for projecting contributions from scratch

- Requires more financial knowledge to use effectively

- Fidelity's interface pushes toward account opening

Who It's For

Anyone with an existing traditional IRA or 401(k) who is seriously evaluating a Roth conversion. Especially valuable for people in their 50s and early 60s in low-income years — for example, early retirees who haven't started Social Security distributions yet and have a window to convert at lower tax rates.

Charles Schwab Roth vs. Traditional IRA Calculator: Best for Tax Bracket Comparison

The Charles Schwab Roth vs. Traditional IRA Calculator is built specifically to answer the question that trips up most retirement savers: should I contribute to a Roth or a traditional IRA? The answer depends almost entirely on whether your tax rate is higher now or will be higher in retirement — and Schwab's calculator makes that comparison concrete and visual.

The tool asks for your current income, tax filing status, annual contribution amount, years until retirement, and expected tax rate in retirement. It then runs both accounts side by side — showing the pre-tax traditional IRA versus the after-tax Roth IRA — and calculates which account leaves you with more money after taxes at retirement. It also shows the cumulative tax savings from each approach.

What distinguishes this calculator from the field is its side-by-side after-tax comparison. Most Roth IRA calculators show only the Roth outcome. Schwab shows you both simultaneously, which makes the decision much cleaner. If your current federal bracket is 22% and you expect to be in the 12% bracket in retirement, the traditional IRA usually wins. If you're in the 12% bracket now and expect to be in the 22% bracket at 70 (thanks to RMDs and Social Security), the Roth usually wins. Schwab's tool quantifies exactly how much each scenario is worth.

The calculator also models the 2026 current contribution limits and is updated for the current tax year. One strong practical use case: a 35-year-old teacher earning $58,000 who wants to know definitively whether to open a Roth or fund a traditional IRA. Schwab's calculator gives them both projections in under 60 seconds and shows the dollar difference between the two outcomes.

Pros

- Roth vs. Traditional side-by-side after-tax comparison

- Accounts for current and projected tax rates

- Clean visual output with easy-to-read charts

- No login required

- Updated to reflect current contribution limits

Cons

- Requires you to estimate your retirement tax rate — which many people find difficult

- No year-by-year breakdown

- No Roth conversion analysis

Who It's For

Anyone sitting on the fence between a Roth IRA and a traditional IRA. Particularly useful for people in the middle income brackets (22%–24%) who genuinely aren't sure which account will produce the better after-tax outcome given their likely retirement income.

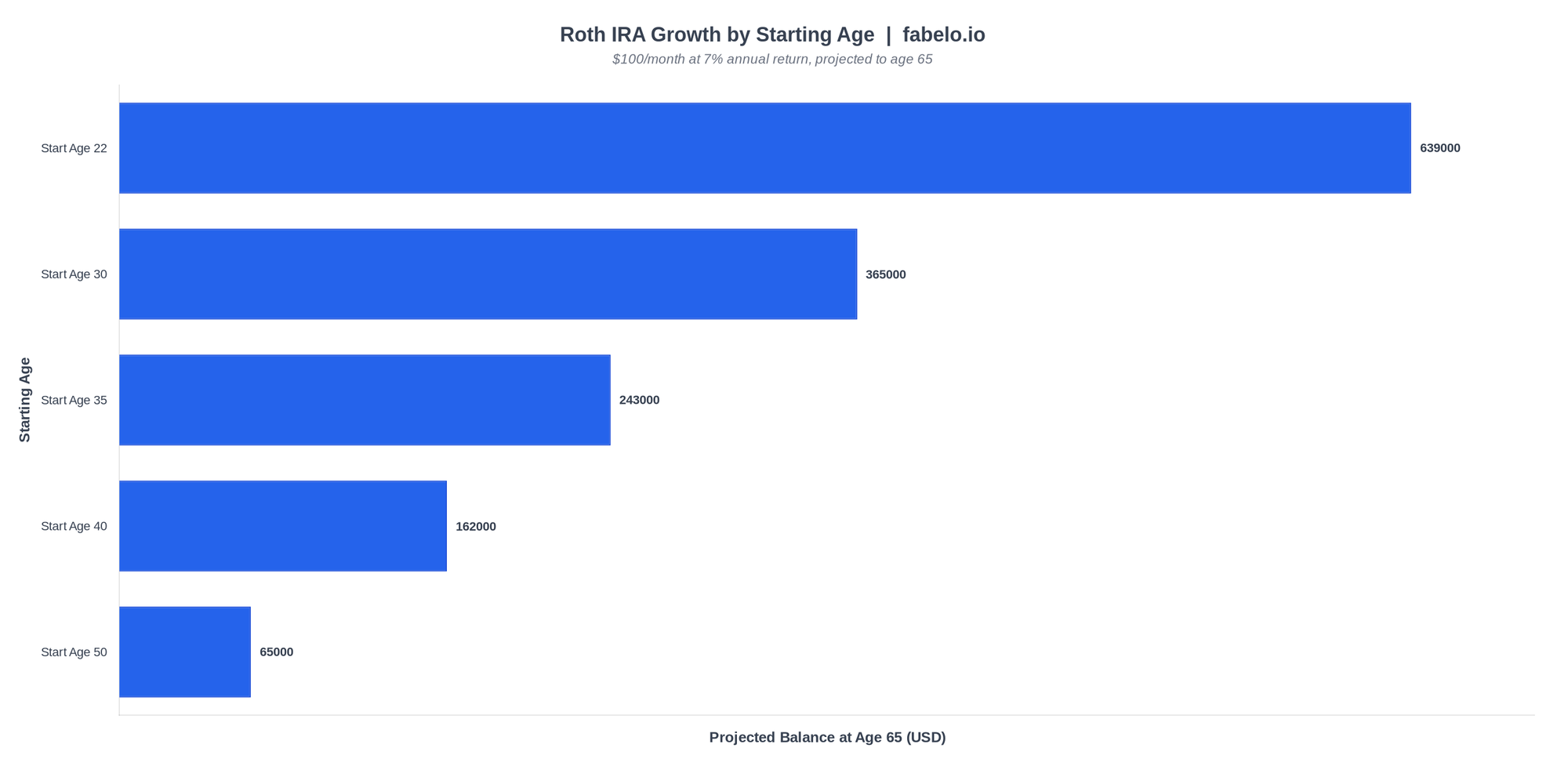

| Starting Age | Years Investing | Total Contributions | Projected Balance at 65 | Earnings (Compounding Gain) |

|---|---|---|---|---|

| 22 | 43 years | $103,200 | $639,000 | $535,800 |

| 30 | 35 years | $84,000 | $365,000 | $281,000 |

| 35 | 30 years | $72,000 | $243,000 | $171,000 |

| 40 | 25 years | $60,000 | $162,000 | $102,000 |

| 50 | 15 years | $36,000 | $65,000 | $29,000 |

Landmark Credit Union Roth IRA Calculator: Best for Credit Union Members

The Landmark Credit Union Roth IRA calculator is a straightforward, no-login tool that covers the basics well. You enter your initial investment, monthly contribution, expected annual return, and number of years. It projects your ending balance and shows a visual summary of contributions versus growth — the classic split that shows how much of your final balance you actually put in versus how much came from compounding.

What sets this calculator apart from the other free tools in this category is its emphasis on the contribution-vs.-earnings split visualization. For most long-term Roth IRA investors, the final account balance consists of far more compounding gains than actual contributions. A 30-year investor contributing $300/month might deposit around $108,000 total — but their ending balance at a 7% return would be roughly $365,000. That means nearly $257,000 of their balance came from earnings, not money out of their pocket. Landmark's calculator makes this split immediately visible in a clear graphical format, which is genuinely motivating for new investors who don't yet grasp how compounding works over long time horizons.

This pairs naturally with a deeper understanding of how compound interest actually works — the mechanics behind why that earnings split looks so dramatic after 30 years.

The tool doesn't model income limits, Roth vs. Traditional comparisons, or Roth conversions. It's a pure growth projection calculator, but it's well-designed and loads reliably without any account creation. Credit union members who want a quick, visual gut-check on their Roth IRA contributions will find this tool satisfying and easy to share with a spouse or financial partner.

Pros

- Strong visual breakdown of contributions vs. Earned growth

- Fast, clean interface

- No login required

- Great for visual learners

Cons

- No income phase-out calculation

- No Roth vs. Traditional comparison

- Fewer input fields than most tools on this list

Who It's For

Visual learners and credit union members who want to quickly see the compounding story behind their Roth IRA contributions. Great for couples reviewing retirement savings together who want a picture, not a spreadsheet.

Roth IRA Calculator by Age: What the Numbers Actually Look Like

One of the most useful things a Roth IRA calculator by age can show is how dramatically starting age affects your final balance. The math is unambiguous: the earlier you start, the more your account balance is dominated by compounding gains rather than contributions. Here's what a $200/month contribution at 7% average annual return looks like at different starting ages, modeled to a common retirement age of 65.

The table below uses a 7% assumed annual return, $200/month contribution, $0 starting balance, and a retirement age of 65 for all scenarios.

| Starting Age | Total Contributions | Projected Balance at 65 |

|---|---|---|

| Age 22 | $103,200 | $639,000 |

| Age 30 | $84,000 | $365,000 |

| Age 35 | $72,000 | $243,000 |

| Age 40 | $60,000 | $162,000 |

| Age 50 | $36,000 | $65,000 |

The 8-year difference between starting at 22 versus 30 costs you roughly $274,000 in final balance — even though the 22-year-old only contributed $19,200 more in total. That gap is almost entirely compounding. Starting at 22 and contributing $200/month produces a final balance nearly 4 times larger than starting at 50 with the same monthly amount.

The question "what does $100 a month in a Roth IRA for 30 years produce?" is one of the most searched retirement planning queries. At 7% annual return, $100/month for 30 years grows to approximately $121,000. That's roughly $36,000 in actual contributions and $85,000 in compounding gains. Increase the contribution to $500/month under the same assumptions and the 30-year total hits about $605,000 — with over $425,000 from compounding alone.

If you're thinking about how Roth IRA growth fits into a larger savings picture, it's worth understanding how this stacks up against other vehicles. Our guide on high-yield savings accounts covers the short-term savings side of the equation.

Quick Comparison of the Best Free Roth IRA Calculators

| Calculator | Best For | Income Phase-Out Check | Roth vs. Traditional | Year-by-Year Breakdown | Login Required |

|---|---|---|---|---|---|

| Bankrate | Beginners | No | No | No | No |

| Calculator.net | Detailed projections | No | Partial (taxable vs. Roth) | Yes | No |

| NerdWallet | Contribution limit check | Yes | No | No | No |

| Fidelity | Roth conversion analysis | N/A | Yes (conversion focused) | Partial | Optional |

| Charles Schwab | Roth vs. Traditional decision | No | Yes | No | No |

| Landmark CU | Visual growth split | No | No | No | No |

Watch This First: Roth Conversions, Tax Strategy, and the Numbers That Matter

Before you run your numbers through any calculator, there's a strategic layer most Roth IRA calculators completely ignore: your tax bracket timing. The Watch: the Ari Taublieb CFP® YouTube channel on Roth conversions and 2026 retirement numbers ? breaks down a real-world case — a 57-year-old with $2 million mostly in a pre-tax 401(k) — and shows how strategic Roth conversions during low-income years between retirement and Social Security can save tens of thousands in taxes. The key insight from the channel's analysis: if your current tax rate is historically low and you have buffer room in your bracket, converting even a small amount to Roth now can capture that bracket permanently, before RMDs and Social Security push you into a higher tier.

One specific warning from the Ari Taublieb CFP® YouTube channel that most Roth IRA calculators don't model: the Medicare IRMAA surcharge. If you do a Roth conversion at age 63, the IRS applies a two-year look-back rule — meaning that conversion income shows up on the tax return Medicare uses to calculate your premiums at age 65. Converting aggressively without accounting for this can spike your Medicare costs by thousands of dollars per year. Standard Roth IRA growth calculators don't flag this at all. If you're within 10 years of Medicare eligibility, factor IRMAA thresholds into any conversion analysis before you run the numbers.

What Real People Are Saying About Roth IRA Calculators

In r/personalfinance, users regularly use free calculators to test specific contribution scenarios. One frequently cited example: setting contributions to $50/week for 25 years with a 7% return assumption — the calculator outputs approximately $177,000. That kind of quick-run helps people conceptualize what modest, consistent contributions actually produce over a career — and it reframes "I can't afford to invest much" into "I can afford $50/week." The community consistently recommends compound interest calculators as a motivational tool, not just a planning tool.

Users in r/personalfinance also frequently ask how much they need to contribute monthly to reach $1 million. The answer depends heavily on starting age and assumed return — a 25-year-old needs roughly $340/month at 7% to hit $1M by 65, while a 35-year-old needs around $700/month under the same assumptions. Running these scenarios in a free Roth IRA calculator takes under a minute and gives people a concrete monthly target to work toward.

In r/personalfinance, one user raised a legitimate limitation that most free calculators don't address: how to model future balance when you plan to increase contributions over time as your salary grows. The honest answer is that most free calculators assume a flat contribution amount. If you want to model escalating contributions — say, starting at $200/month and increasing by 3% annually — you either need a spreadsheet or a paid planning tool. Knowing this limitation upfront saves frustration when you're trying to model a more realistic career savings trajectory. This connects directly to how the compound interest formula handles variable periodic inputs versus fixed ones.

Users in r/DaveRamsey often reference the 15% gross income savings benchmark — the idea being that contributing 15% of your gross income across all retirement accounts is a reasonable target for most people to retire comfortably. A Roth IRA alone can rarely absorb that full amount given the annual contribution caps, but it's a useful framework for understanding whether your total retirement savings rate is on track.

How We Chose the Best Roth IRA Calculators

Our analysis focused on six specific criteria. We tested each calculator by running identical inputs — 35-year-old, $0 starting balance, $400/month contribution, 7% return assumption, retirement at 65 — and evaluated both the output quality and the user experience. Tools were excluded if they required account creation to view results, if they embedded undisclosed assumptions, or if their output couldn't be cross-verified against standard compound interest math.

We excluded several bank-branded calculators (Valley Bank Glacier, Farmers State Bank) that appeared in search results because their tools produced identical outputs to the or Calculator.net engines with no meaningful differentiation. White-labeled calculators that are exact copies of third-party tools add no value to a comparison — users are better served going directly to the original source.

We also excluded any calculator that hadn't been updated to reflect the current IRS contribution limits. The 2024 standard Roth IRA contribution limit is $7,000 ($8,000 if you're 50 or older under the catch-up provision). Tools that still defaulted to older limits were removed from consideration for accuracy reasons.

| Evaluation Criterion | What We Looked For | Weight |

|---|---|---|

| Output accuracy | Results match standard compound interest formula verification | High |

| Input flexibility | Allows monthly vs. Annual, starting balance, adjustable return rate | High |

| IRS current limits | Updated to reflect 2024–2026 contribution and phase-out limits | High |

| User experience | No login wall, fast load time, mobile-accessible | Medium |

| Unique feature value | Offers something no other calculator in this list provides | Medium |

| Source transparency | Calculator discloses assumptions and methodology to users | Medium |

Tools from major brokerage platforms (Fidelity, Schwab) were included despite their potential upsell context because their calculators offer genuinely differentiated functionality — specifically the conversion analysis and the Roth vs. Traditional comparison — that pure third-party tools don't replicate. The presence of account-opening prompts doesn't disqualify a tool if the calculator itself is accurate and useful.

Frequently Asked Questions About Roth IRA Calculators

How accurate is a free Roth IRA calculator compared to what a financial advisor would project?

Free calculators use the same underlying compound interest math a financial advisor uses for basic projections. The gap between a free tool and professional advice isn't in the formula — it's in the inputs. A CFP accounts for inflation adjustments, variable contribution amounts, Social Security integration, required minimum distribution planning, and tax bracket optimization over time. A free calculator assumes fixed contributions and a constant return rate. For ballpark planning and motivation, free tools are accurate. For decisions involving six or seven figures, the calculator is a starting point — not the final answer.

What return rate should I use in a Roth IRA growth calculator if I'm investing in index funds?

The S&P 500 has historically averaged roughly 10% annually before inflation, or about 7% after adjusting for inflation. Most financial planners use 6–7% as a conservative real return assumption for long-term projections. Using 7% is reasonable for a stock-heavy portfolio with a 20+ year horizon. Using 5–6% is more conservative and accounts for years you might shift toward bonds as you approach retirement. Don't use 10% for long-term planning — it overstates likely after-inflation outcomes.

Can I use a Roth IRA calculator if I'm in the income phase-out range and my contribution is reduced?

Yes, but you need to calculate your reduced contribution limit first and then enter that number. The IRS formula for the phase-out reduces your maximum contribution by a specific dollar amount per dollar of income above the threshold. For 2024, single filers with MAGI between $146,000 and $161,000 have their contribution limit reduced proportionally. Use the Roth IRA calculator — it calculates this reduced limit automatically before running the growth projection. Once you have your eligible contribution amount, any of the other calculators will work with that number.

If I contribute $100 a month to a Roth IRA for 30 years, what will my balance be at retirement?

At a 7% average annual return, $100/month for 30 years grows to approximately $121,000. Your total out-of-pocket contributions would be $36,000 — meaning roughly $85,000 of that final balance came from compounding growth, not money you deposited. At a 6% return, the same scenario produces about $100,400. At 8%, you'd be looking at approximately $149,000. Every dollar of additional monthly contribution adds roughly $1,200 to that 30-year outcome under 7% assumptions.

Does a Roth IRA calculator account for the 5-year rule on tax-free withdrawals?

No standard free Roth IRA calculator models the 5-year rule, and they don't need to for long-term projections. The 5-year rule requires that a Roth IRA be open for at least 5 tax years before earnings can be withdrawn tax-free. For anyone opening a Roth IRA in their 20s, 30s, or 40s and planning to withdraw at retirement age, this rule is almost never a practical constraint — by retirement you'll have had the account open for decades. It only becomes relevant if you open a Roth IRA in your late 50s or make a Roth conversion close to retirement age.

Can I use a Roth IRA calculator to figure out how much I need to contribute monthly to reach $1 million?

Yes — this is one of the most useful reverse-engineering applications of these tools. Most calculators don't have a "solve for contribution" mode, so you'll need to adjust the monthly input manually until you hit your target. At 7% return, a 25-year-old needs approximately $340/month for 40 years to reach $1 million. A 30-year-old needs roughly $530/month. A 35-year-old needs about $820/month. The IRS annual contribution limit ($7,000 in 2024, or about $583/month) caps how fast you can get there within a Roth IRA alone — which is why many investors max out their Roth and then continue investing in a taxable brokerage.

Should I use a Roth IRA calculator before or after I decide whether to do a Roth conversion?

Use a Roth conversion calculator first (Fidelity's is the best free option), then use a Roth IRA growth calculator to model what the converted balance will produce from that point forward. The conversion decision is a tax question — will you pay more in taxes converting now or taking distributions later? The growth projection is a compounding question — what does this balance become over time? They're sequential decisions. Don't run a Roth IRA growth calculator on pre-conversion assets and assume that answers the conversion question.

Final Verdict

The best free Roth IRA calculator for most people is 's. It's fast, accurate, requires no login, and gives beginners exactly what they need: a clean growth projection based on real inputs. For anyone who wants a year-by-year breakdown, Calculator.net is the deeper tool. For higher earners who need to verify eligibility, 's income phase-out integration is the right starting point. For Roth conversion decisions specifically, Fidelity's conversion calculator is the only free tool that models the tax break-even analysis with any real depth.

The takeaway from running these tools together: starting early matters more than the contribution amount, and the tax-free nature of Roth IRA growth is most valuable for people in lower tax brackets now who expect higher income (or RMD-driven income) in retirement. A Roth IRA calculator helps you see that value in dollar terms — not just in theory.

Bottom line: Use a Roth IRA growth calculator to set a monthly contribution target, use to verify you're eligible, and use Fidelity's tool if you're considering moving pre-tax money into a Roth. The math takes five minutes. The results give you a retirement target worth building toward. If you're working on your overall retirement savings approach, our guide on zero-based budgeting helps you find the monthly cash flow to actually fund these contributions consistently.

About the Author

Written by Varn Kutser

Personal finance writer covering savings, investing, and budgeting with a data-first approach. Every rate, limit, and claim is verified against official sources — FDIC, IRS, and Federal Reserve. No clickbait, no guesswork, just numbers.

Disclaimer: Rates and terms mentioned in this guide are subject to change. Verify current rates directly with financial institutions before opening any account.

Last updated: April 22, 2026 · fabelo.io