How To Build Wealth in Your 20s: A Complete Step-by-Step Guide

Building wealth in your 20s comes down to 7 steps: fix your income, protect your margin, kill high-interest debt, invest early, and use tax-advantaged acco

Building wealth in your 20s comes down to one non-negotiable sequence: fix your income first, protect the gap between what you earn and spend, eliminate high-interest debt, then invest consistently in tax-advantaged accounts. People who start at 22 instead of 32 end up with 2–3 times more wealth by retirement — not because they were smarter, but because compounding had a decade more to run. The steps below are ordered deliberately. Skip the sequence and you slow everything down.

Savings estimates and compounding examples in this guide are based on historical market averages, national household spending data, and community-reported figures. Actual results vary by income, location, and investment choices.

This is not a motivation piece. Every step here is actionable, sequenced for real 20-somethings — whether you're earning $35,000 or $90,000 a year. The math works at almost every income level if you follow the order.

Contents

- Step 1: Solve the Income Problem First

- Step 2: Protect the Gap Between Income and Spending

- Step 3: Build Your Emergency Fund and Kill High-Interest Debt

- Step 4: Start Investing Early, Even If the Amounts Feel Small

- Step 5: Layer In Tax-Advantaged Accounts

- Step 6: Diversify and Build Multiple Income Streams

- Step 7: Automate Everything and Raise Your Financial Floor

- Wealth Building Methods Compared

- Watch This First

- What Real People Are Saying

- Frequently Asked Questions

- Your Next Steps

Step 1: Solve the Income Problem First

You cannot save and invest your way out of a bad income. This is the foundational truth that most personal finance content glosses over. If you're earning $30,000 a year with $28,000 in expenses, no budgeting app in the world fixes that math. The first move in learning how to build wealth in your 20s is to make your income the priority — everything else is downstream from it.

Start by identifying a high-value skill the market will pay for. This doesn't require a four-year degree. Sales, digital marketing, software development, skilled trades, data analysis, and project management all offer strong starting salaries and clear growth paths. The question to ask is simple: what skill, if mastered in 12–18 months, would add $10,000–$20,000 to your annual income? That's a better ROI than almost any investment you'll make in your 20s.

Side income matters here too, especially early on. The extra cash flow — even $500–$800 a month — goes straight into your investment pipeline, not your lifestyle. For ideas on where to start, the side hustle ideas for beginners guide covers specific options with realistic earning potential. The goal isn't to run yourself ragged. The goal is to create enough margin that investing becomes possible, not theoretical.

Income also determines how aggressively you can pursue steps 4 and 5 below. A person earning $70,000 who maxes a Roth IRA ($7,000/year) and captures a full 401(k) employer match is building serious tax-advantaged wealth. Someone earning $32,000 might only be able to contribute $100/month to start — and that's fine, as long as the habit exists and grows. The key is that your income trajectory trends upward throughout your 20s, not flat.

Salary negotiation is one of the fastest income levers available. Most people leave significant money on the table in their first three job offers simply because they don't negotiate. A well-constructed salary negotiation email can add $3,000–$8,000 to your base salary — which compounds across every future raise and bonus calculation.

Step 2: Protect the Gap Between Income and Spending

Wealth is built in the gap between what you earn and what you spend. Not in the stock market. Not in crypto. In the gap. The market is just where you deploy what the gap produces. This is the single most underrated principle in personal finance for people in their 20s, and it's the one most people violate the moment their income rises.

Lifestyle inflation is the silent wealth killer. You get a $5,000 raise and upgrade your apartment. You land a promotion and start eating out four nights a week instead of two. Each individual choice seems reasonable. Collectively, they eliminate the margin that should be funding your future. The most financially effective people in their 20s keep their lifestyle 12–24 months behind their income — intentionally.

A practical framework: every time your income increases, direct at least 50% of the net increase toward savings or investing before adjusting any spending. If your take-home pay rises by $400/month, $200 goes to your investment accounts automatically and the remaining $200 is available for lifestyle. This "pay yourself first on every raise" habit is what separates people who feel broke at $85,000 from people who are genuinely building wealth at $55,000.

Structuring your budget around a clear framework helps enormously here. The zero-based budgeting method assigns every dollar a job before the month starts — which makes lifestyle creep visible instead of invisible. When you can see exactly where each dollar is going, you make different choices. Tools like YNAB and EveryDollar are built specifically for this approach.

For more detailed strategies on keeping spending low without misery, the frugal living tips guide covers tactics that actually stick long-term — focused on high-impact cuts, not deprivation.

Step 3: Build Your Emergency Fund and Kill High-Interest Debt

Before you invest a single dollar in the market, two things need to be in place: a funded emergency reserve and zero high-interest consumer debt. Skip this step and every market downturn or unexpected expense becomes a crisis that forces you to liquidate investments at exactly the wrong time.

Your emergency fund should cover 3–6 months of essential expenses. If your fixed costs (rent, utilities, food, insurance, transportation) run $2,800/month, you need $8,400–$16,800 parked somewhere accessible but separate from your checking account. A high-yield savings account is the right vehicle for this — you earn meaningful interest while keeping the money liquid and FDIC-insured.

All rates and APYs mentioned in this guide are for illustration purposes. Rates change frequently — always verify current rates directly with your financial institution before making decisions.

High-interest debt — anything above roughly 8–10% APR — destroys wealth faster than most investments can create it. A credit card charging 22% APR is a guaranteed 22% drag on every dollar you carry. No index fund delivers a consistent 22% return. The math is simple: pay off high-interest debt before investing in anything beyond capturing your employer's 401(k) match (more on that in Step 5). If you're dealing with multiple high-rate balances, the debt consolidation options guide explains how to lower your effective interest rate while paying down principal faster.

Student loans at 4–6% and mortgages sit in a different category — these can coexist with investing because the interest rate is low enough that market returns typically exceed them. The dividing line is roughly 8%. Above that, pay it off. Below that, invest while making minimum payments.

The sequence — emergency fund first, then high-interest debt — matters because the emergency fund prevents you from going back into high-interest debt the moment something breaks. One $1,500 car repair shouldn't derail a year of wealth building. With a funded reserve, it doesn't.

Step 4: Start Investing Early, Even If the Amounts Feel Small

Compounding is why investing in your 20s is a more powerful tool to build wealth than saving alone — by a significant margin. A dollar invested at 22 has roughly 43 years to compound before a standard retirement age. The same dollar invested at 32 has 33 years. That 10-year difference, at a historical average annual return of around 7–10% in a diversified equity portfolio, produces dramatically different outcomes.

Consider the math: $200/month invested starting at 22, assuming a 7% average annual return, grows to approximately $525,000 by age 65. Start the same $200/month at 32 and you arrive at roughly $243,000 — less than half. The amount invested is similar. The difference is entirely time. Understanding the full mechanics of this is worth studying — the compound interest calculator guide breaks down exactly how these numbers work so you can run your own scenarios.

For early investors, keep it simple. An S&P 500 index fund or a total market ETF gives you broad diversification at near-zero cost. The expense ratio on a Vanguard or Fidelity index fund is typically 0.03–0.05% annually — essentially free. Avoid individual stock picking until you have a solid base built. The goal at this stage is momentum and habit, not optimization. You can always refine your allocation as your knowledge and portfolio grow. For a clear breakdown of the options available, the index funds vs ETF comparison covers the key differences in plain language.

According to discussions in r/Rich, people who built meaningful net worth in their 20s consistently point to one habit above all others: they started investing before they felt ready. Waiting until you have the "right" amount or the "right" knowledge is one of the most expensive delays you can make. Start with whatever you can — $50, $100, $200 a month — and increase it as your income grows.

Step 5: Layer In Tax-Advantaged Accounts

Tax-advantaged accounts are one of the most powerful and underused tools for anyone figuring out how to start building wealth at 25 or any point in their 20s. The government has created explicit incentives for long-term investing — your job is to use every one of them.

Start with your employer's 401(k), specifically the match. If your employer matches up to 4% of your salary, contribute at least 4%. Not doing so is leaving part of your compensation on the table. A $50,000 salary with a 4% match means your employer will contribute $2,000/year to your retirement — free money that compounds for decades.

Next, open a Roth IRA if your income qualifies. The Roth is particularly powerful for people in their 20s because you're likely in a lower tax bracket now than you will be later. You contribute after-tax dollars today, and everything — contributions and growth — comes out tax-free in retirement. The Roth IRA contribution limits guide covers the current annual limits and income thresholds, which the IRS adjusts periodically.

The priority order for tax-advantaged investing looks like this:

- 401(k) contributions up to the employer match (free money first)

- Max your Roth IRA if income-eligible

- Return to your 401(k) and contribute beyond the match if you have additional margin

- Taxable brokerage account for anything beyond those limits

Health Savings Accounts (HSAs) are worth mentioning if you're on a high-deductible health plan. An HSA offers a triple tax advantage — contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. Unused funds roll over every year and can be invested. At 65, you can withdraw for any purpose without penalty (just ordinary income tax applies), making it function as a stealth IRA.

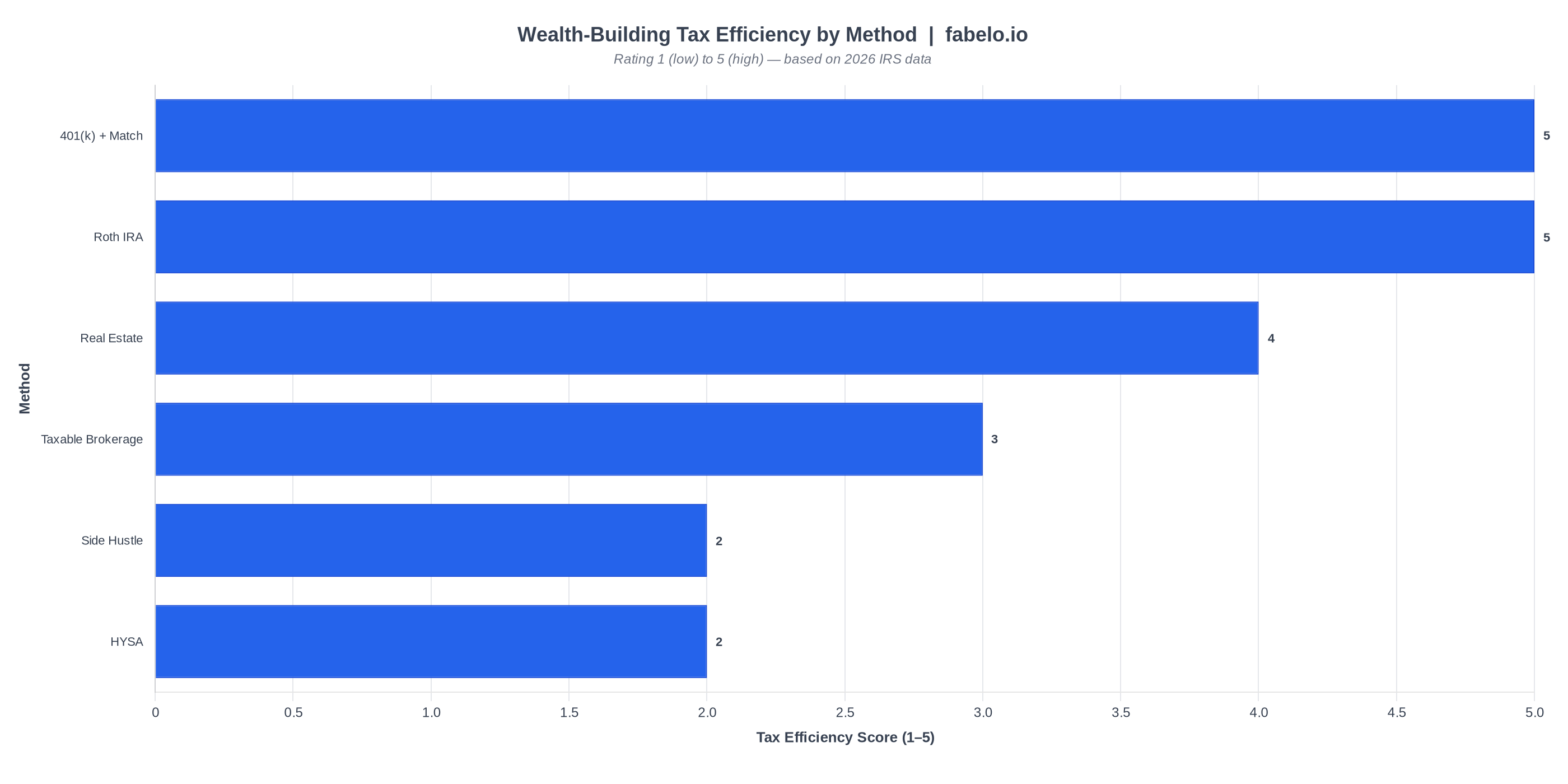

| Method | Time to Results | Min. Capital to Start | Tax Efficiency (1–5) | Effort Level |

|---|---|---|---|---|

| 401(k) + Employer Match | Long-term (20–40 yrs) | $0 (% of paycheck) | 5 | Low (set and forget) |

| Roth IRA (Index Funds) | Long-term (20–40 yrs) | $1 (most brokers) | 5 | Low |

| Taxable Brokerage Account | Medium-term (5–15 yrs) | $1 | 3 | Low to Medium |

| Real Estate (House Hack) | Medium to Long-term | $10,000–$30,000+ | 4 | High |

| Side Hustle / Freelancing | Short-term (weeks) | $0–$500 | 2 | High (initially) |

| High-Yield Savings Account | Immediate | $1–$100 | 2 | Minimal |

Step 6: Diversify and Build Multiple Income Streams

A single income source is a single point of failure. One of the clearest patterns among people who reach significant net worth in their 20s is that they build income from at least two directions. This isn't about running five side hustles at once — it's about creating a second stream that grows without requiring proportional time input.

The most practical second income streams for people in their 20s fall into a few categories. Freelancing in your primary skill area (writing, design, coding, consulting) is the fastest to monetize — you're selling what you already know. Digital products, content creation, and rental income take longer to build but can generate revenue without trading hours directly. For a structured breakdown of options that work without significant upfront capital, the passive income online guide covers realistic starting points.

On the investment side, diversification means not concentrating everything in a single asset class, sector, or geography. A portfolio of mostly U.S. Equity index funds is reasonable and simple for early investors. As your balance grows past $50,000–$100,000, it's worth adding international exposure and potentially some bond allocation — not because bonds outperform stocks long-term, but because they reduce volatility during downturns, which matters more as your portfolio gets larger.

Real estate is another avenue some 20-somethings pursue, particularly through house hacking — buying a duplex or small multi-family property, living in one unit, and renting the others. Done correctly, tenants effectively cover your mortgage while you build equity. It requires more capital upfront and more active management than index fund investing, but the leverage available in real estate can accelerate wealth building meaningfully for the right person in the right market.

The key principle across all diversification is this: don't diversify into things you don't understand. A complex options strategy or a niche crypto asset isn't diversification — it's speculation. Start broad, stay simple, and add complexity only as your understanding grows.

Step 7: Automate Everything and Raise Your Financial Floor

Willpower is a terrible financial system. The most consistent wealth builders in their 20s remove willpower from the equation entirely by automating every key financial behavior. When saving and investing happen automatically before you can spend the money, the decision is made once instead of every month.

Set up automatic transfers on the day after your paycheck hits. This means: automatic transfer to your emergency/savings account, automatic 401(k) contribution (typically set through your HR portal), and automatic investment into your Roth IRA or brokerage account. What's left after automation is your actual spending budget — not theoretical, not hoped-for, but real. The paycheck budgeting guide covers how to sequence these transfers so nothing gets missed.

Raising your financial floor means making your minimum baseline more secure over time. This includes building your credit score (which lowers borrowing costs for a mortgage or business loan later), maintaining adequate insurance coverage (a single medical emergency without insurance can wipe out years of savings), and keeping your fixed costs low relative to income even as income grows.

Credit score management in your 20s is often overlooked as a wealth-building tool, but a score above 750 can save tens of thousands of dollars in interest over the life of a mortgage. The mechanics are simple: pay balances in full monthly, keep utilization below 30%, don't close old accounts, and avoid applying for multiple credit products in a short window.

Finally, review your financial system every six months. Income changes, expenses shift, and contribution limits adjust. What worked at 22 needs refinement at 26. Build the habit of a twice-yearly financial review — 30 minutes to check whether your automation is still calibrated to your current income and goals.

Wealth Building Methods Compared

Not all wealth-building approaches deliver equal results in your 20s. The table below compares the most common methods across the dimensions that matter most for early-stage wealth building: time to see results, capital required to start, tax efficiency, and effort level.

The table above makes one pattern clear: the highest tax-efficiency vehicles (401k and Roth IRA) also require the least effort — which is exactly why they should anchor every 20-something's wealth strategy. Side hustles and real estate can accelerate the timeline but demand significantly more active input.

Watch This First

According to the Mat Sorensen - Wealth Lawyer and Entrepreneur YouTube channel, the most critical and consistently violated principle in wealth building is the order of operations. Most people fail not because they chose bad investments, but because they invested before eliminating high-interest debt or establishing reserves — meaning every market dip or life expense forced them to liquidate at a loss. The video is particularly clear on why momentum in the early stages matters more than perfect investment selection: getting money working for you — even in a basic S&P 500 index fund — beats paralysis from over-analysis every time.

The channel also makes a compelling case for the gap protection principle: a doctor in the video's example retired at 45 not because of exceptional investment performance, but because he kept his lifestyle frozen at a "medical student" level for five years after his income jumped dramatically. The gap between his growing income and his stable expenses funded a compounding machine. This isn't unique to high earners — the same logic applies at any income level. Protect the gap first. Let compounding do the math over time.

What Real People Are Saying

Reddit communities focused on personal finance are unusually candid about what actually works — and the consensus across several threads is sharper than most published advice.

In r/Money, users discussing how to use their 20s effectively consistently land on the same point: trimming monthly fixed costs early creates an extra decade of compounding that no investment strategy can replicate later. Several commenters in the thread noted that moving back home temporarily, getting a roommate, or driving an older car for a few years produced more long-term wealth than any market pick they'd made.

In r/EntrepreneurRideAlong, a thread on building wealth without a college degree drew a strikingly practical response from multiple users: max the 401(k) match, max the Roth IRA, avoid debt aggressively, and build marketable skills. No exotic strategies, no leverage plays — just consistent execution of fundamentals.

In r/povertyfinance, where the starting point is genuinely constrained income, users pushed back on investing-first advice: "Focus on earning power first, not investing hacks." The suggestion to build a skill in sales, tech support, trades, or digital marketing before worrying about portfolio allocation reflects the same income-first logic in Step 1 above. The thread is a useful reality check for anyone in a tight financial situation — wealth building at $28,000/year looks different than at $65,000, but the sequence is the same.

In r/Money, a thread asking wealthy people what they'd do differently at 20 drew one answer repeatedly: "Automate your finances and live below your means. Always invest. Start a side hustle and never stop learning." Short, unadorned, and consistent with every data point in this guide.

Frequently Asked Questions

How much money should I have saved and invested by age 25 to stay on track for wealth building?

A common benchmark is having one full year's salary saved or invested by age 30. By 25, aiming for 0.25–0.5x your annual salary in invested assets is a reasonable milestone. More important than any specific number is whether your savings rate is consistently above 15–20% of gross income and trending upward. Someone earning $45,000 at 25 with $8,000 invested and a 20% savings rate is better positioned than someone with $15,000 invested but a 5% savings rate.

Why is investing a more powerful tool to build wealth than saving alone?

Saving preserves money; investing multiplies it. A savings account earning 4–5% APY builds purchasing power modestly, but a diversified equity portfolio historically returns 7–10% annually on average over long periods. At 7%, money doubles roughly every 10 years. At 4%, it doubles every 18. Over a 40-year horizon, the compounding difference is enormous — a $10,000 investment at 7% becomes approximately $149,000, while the same amount in a 4% savings account grows to about $48,000. The gap widens with time, which is exactly why starting in your 20s matters so much.

Can I realistically become a millionaire in my 20s on an average income?

Reaching a $1,000,000 net worth in your 20s on a median American income is statistically rare — but building a foundation that reaches seven figures by your late 30s or 40s is very achievable. Someone earning $55,000 who saves aggressively (20–25% of income), captures their full 401(k) match, and invests consistently from age 22 can reach $1 million by their mid-40s through compounding alone. Learning how to become a millionaire in your 20s is less about timeline and more about building the right habits early. The habits formed in your 20s determine the trajectory of the following three decades.

What's the best first investment account to open if I'm starting wealth building at 25 with no investment experience?

Start with your employer's 401(k) if there's a match — that's an immediate guaranteed return on contribution. If you're self-employed or there's no employer plan, open a Roth IRA with Fidelity, Vanguard, or Schwab and invest in a single total-market or S&P 500 index fund. These brokers have no account minimums and expense ratios near zero. The Roth is particularly valuable at 25 because your tax rate is likely the lowest it will ever be — you're locking in tax-free growth on decades of compounding.

How should I handle student loan debt while trying to build wealth in my 20s?

Federal student loans in the 4–7% range can coexist with investing — you don't need to pay them off before contributing to a 401(k) match or Roth IRA. The math favors investing when your loan rate is below what a diversified equity portfolio historically returns. However, if you have private loans above 8–9% APR, prioritize those the same way you'd treat credit card debt: pay them down aggressively before allocating to taxable investments. Always make minimum payments on all loans regardless to protect your credit score.

How does building wealth in your 20s differ from building wealth in your 30s?

The core principles are identical — income gap, debt management, tax-advantaged investing — but the timeline pressure is different. When learning how to build wealth in your 30s, you have less compounding runway, which means contribution amounts matter more and lifestyle choices need to be more deliberate. Someone starting at 32 typically needs to save 25–30% of income to reach the same outcome as someone who started at 22 saving 15%. Starting in your 20s buys you flexibility; starting in your 30s requires intensity. Neither is too late — but the cost of delay is real and measurable.

Is it better to pay off all debt or start investing in my 20s when I have limited income?

It depends entirely on the interest rate. High-interest debt above 8–10% APR should be eliminated before investing beyond capturing the employer 401(k) match. Below that threshold, invest and service debt simultaneously. The employer match is non-negotiable — it's a 50–100% instant return on contributed dollars, which no debt payoff strategy can match. For structured guidance on sequencing these decisions, the Money Guy's wealth building guide for 20-somethings covers a detailed financial order of operations that maps well to different income levels.

Your Next Steps

The distance between knowing this information and actually building wealth in your 20s comes down to three concrete actions taken in the next 30 days:

- This week: Calculate your current gap — subtract total monthly expenses from take-home pay. If the gap is less than 15% of your gross income, identify one expense to cut or one income move to make before the month ends. The gap is your wealth engine. Size it deliberately.

- Within 14 days: Open a Roth IRA if you don't have one (Fidelity and Schwab have no minimums), log into your 401(k) portal and verify you're contributing at least enough to capture the full employer match, and set up one automatic transfer — even $50 — to a high-yield savings account for your emergency fund. Automation removes the willpower requirement permanently.

- Within 30 days: Run your own compounding scenario using the compound interest calculator with your actual numbers — your current savings rate, your realistic income trajectory, and a 7% assumed average return. Seeing the specific dollar figure you'll have at 45 or 55 based on today's decisions is more motivating than any general advice. Make it concrete, make it yours.

People who look back at their 30s and 40s wishing they'd started earlier all had one thing in common: they knew the steps but waited for the "right time" to start. The right time is the month you stop waiting.

About the Author

Written by Varn Kutser

Personal finance writer covering savings, investing, and budgeting with a data-first approach. Every rate, limit, and claim is verified against official sources — FDIC, IRS, and Federal Reserve. No clickbait, no guesswork, just numbers.

Disclaimer: Rates and terms mentioned in this guide are subject to change. Verify current rates directly with financial institutions before opening any account.

Last updated: April 22, 2026 · fabelo.io