How To Save Money Fast: A Complete Step-by-Step Guide

Want to save money fast? Start by building a bare-bones budget, automating transfers to savings, and cutting 3 recurring expenses this week. Real steps, no

Saving money fast doesn't require a six-figure salary — it requires a system. The most effective approach combines three moves: building a bare-bones budget within 24 hours, automating at least 5% of your paycheck into a separate savings account, and cutting at least three recurring expenses in your first week. Most people who do all three see $200–$500 freed up in month one.

The problem isn't that people don't want to save. It's that they try to save whatever's left over at the end of the month — which is usually nothing. Flip that logic. Pay yourself first, spend what remains, and watch the math work in your favor. Whether you're figuring out how to save money fast on a low income or trying to build a real financial cushion for the first time, the steps below are arranged in order of impact. Start at Step 1 and don't skip ahead.

Savings estimates in this guide are based on national averages, community-reported figures, and published household spending data. Actual savings vary by location, household size, and spending habits.

Contents

- Build a Bare-Bones Budget in One Sitting

- Open a Dedicated Savings Account Today

- Automate Your Savings So Willpower Isn't Required

- Audit and Cut Your Subscriptions This Week

- Slash Your Food Budget Without Going Hungry

- Build Your Emergency Fund First

- Use Clever Ways To Save Money on Every Purchase

- How To Save Money Fast: Methods Compared

- Watch This First

- What Real People Are Saying

- Frequently Asked Questions

- Your Next Steps

Build a Bare-Bones Budget in One Sitting

The single biggest reason people fail to save money fast is that they have no accurate picture of where their money goes. A bare-bones budget fixes that in one session — no apps required, no financial expertise needed. Grab your last two bank statements and a piece of paper, or open a simple spreadsheet.

Start by listing your fixed monthly income after taxes. Then list every expense: rent/mortgage, utilities, car payment, insurance, groceries, subscriptions, dining out, gas, phone, and any minimum debt payments. Add everything up. The gap between income and total expenses is your current "savings potential" — or the deficit you need to close.

The 50/30/20 rule is a useful starting framework. Fifty percent of take-home pay goes to needs (housing, food, utilities, transportation), 30% to wants (dining, entertainment, hobbies), and 20% to savings and debt repayment. If your "needs" are eating 70% or more of your income, that's your immediate target for reduction. For a deeper system, zero-based budgeting assigns every dollar a job so nothing leaks unnoticed.

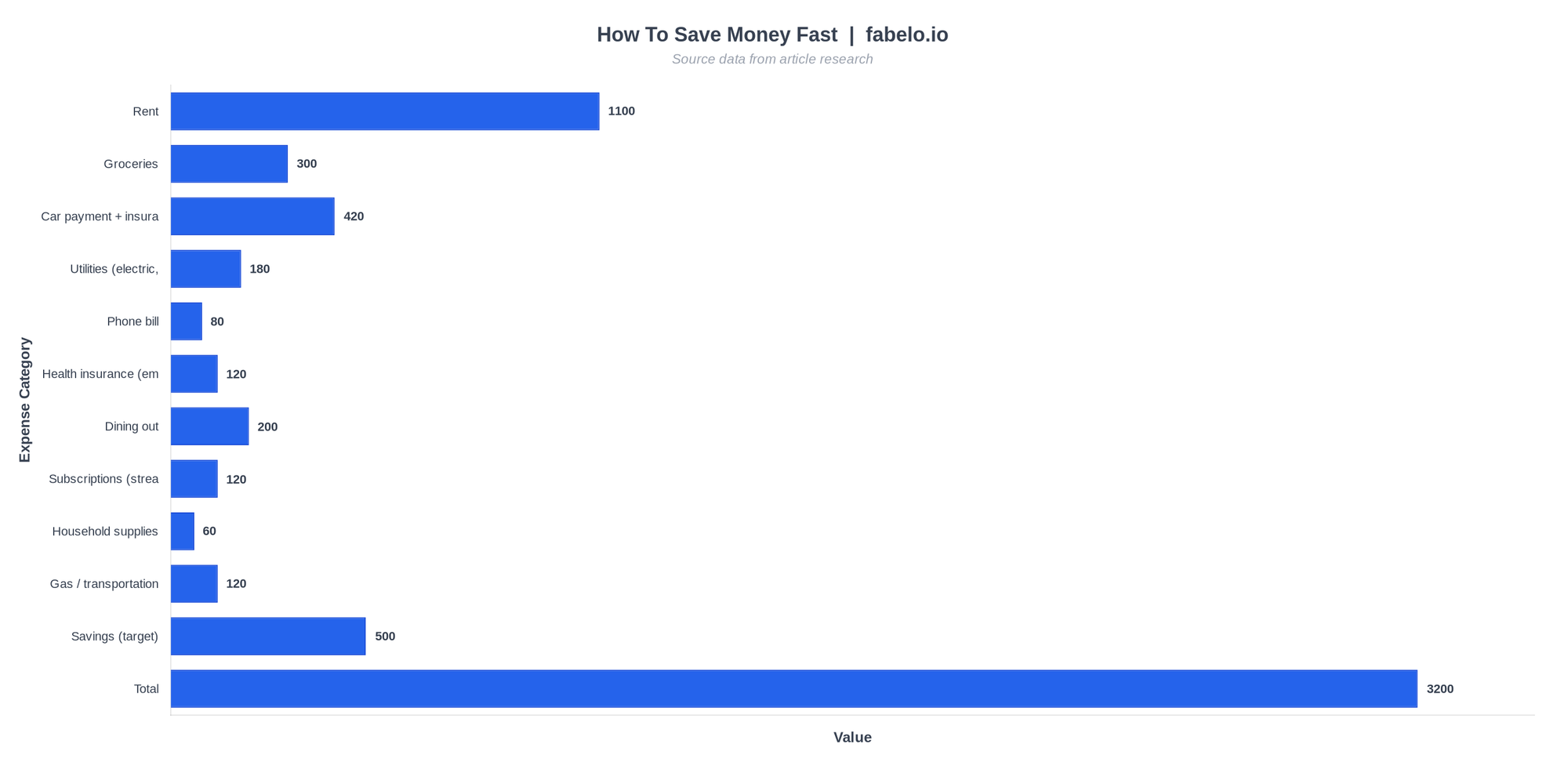

For a real example: someone earning $3,200/month after taxes might find their expenses look like this when they finally write everything down:

Once you can see your money this clearly, you stop wondering where it went. You know exactly which categories to trim. The dining-out and subscription lines are usually the fastest wins — and that's where the next steps focus.

If you want to track this digitally, YNAB and EveryDollar are both built around giving every dollar a purpose. YNAB has a learning curve but is highly effective for people who've struggled with traditional budgets. EveryDollar is simpler and free at the basic level. Also see our full guide on how to budget your paycheck for a more detailed walkthrough.

Open a Dedicated Savings Account Today

Keeping savings in the same checking account as your spending money is a recipe for accidentally spending it. Open a separate, dedicated savings account — ideally a high-yield savings account (HYSA) — and treat it as untouchable except for its intended purpose.

Why a high-yield savings account specifically? Traditional big-bank savings accounts often pay next to nothing in interest. High-yield savings accounts at online banks routinely offer significantly higher returns. That difference compounds meaningfully over time — and if you want to understand exactly how, the compound interest calculator guide breaks it down with real numbers.

All rates and APYs mentioned in this guide are for illustration purposes. Rates change frequently — always verify current rates directly with your financial institution before making decisions.

The psychological separation matters just as much as the interest rate. When your savings live in a different account — ideally at a different bank with a slight delay to transfer funds back — the friction of spending it prevents impulse withdrawals. Out of sight genuinely means out of mind for most people. Read the full breakdown of high-yield savings accounts to compare current options and find one that fits your situation.

Opening an account takes under 10 minutes at most online banks. You typically need a Social Security number, a government-issued ID, and a small initial deposit (sometimes as low as $1). Do it today — not this weekend, not next week. The account sitting open and empty is the first step to filling it.

Automate Your Savings So Willpower Isn't Required

Automation is the most reliable saving strategy ever invented. It removes the decision entirely. When you have to actively choose to transfer money to savings each month, life gets in the way — an unexpected bill, a social event, a bad week. When the transfer is automatic, it happens regardless.

Set up a recurring transfer from your checking account to your savings account on the same day your paycheck hits. Even if it's $50 or $100 to start. The amount matters less than the habit. Once you've proven to yourself that you can live without that money, increase the transfer amount by $25–$50 every 60–90 days.

If your employer allows direct deposit splitting, use it. Have a fixed dollar amount sent directly to savings and the rest to checking. This is even cleaner than a scheduled transfer because the money never touches your spending account at all. You never "see" it, so you never miss it. Many people who struggle with consistent saving find this single change more effective than any budgeting app or financial plan.

Start small if you're on a tight income. Even $25 per paycheck adds up to $650 a year on a biweekly pay schedule — and that's before any interest. Compound growth makes that number grow faster the longer it stays invested. The key is starting now rather than waiting for the "perfect" amount.

Audit and Cut Your Subscriptions This Week

Subscription creep is real. Most Americans underestimate their total monthly subscription spending by 40–80%. You sign up for a free trial, forget to cancel, and pay $14.99 for three years without ever using the service. Go through every line item on your last two credit card and bank statements and flag anything recurring.

Common subscriptions people forget they're paying for include multiple streaming services, unused gym memberships, app subscriptions (cloud storage, VPNs, productivity tools), magazine or news subscriptions, and subscription boxes. For each one, ask: Did I use this in the last 30 days? If the answer is no, cancel it today — not after you "try it one more time."

The average household can free up $50–$150/month just from canceling subscriptions they don't actively use. That's $600–$1,800 per year redirected to savings without changing your lifestyle in any meaningful way. If you're working on how to save money fast on a low income, this step is especially high-leverage because it requires zero income change — just a few minutes of cancellation clicks.

For subscriptions you actually use but could replace for less, look for alternatives. Many free or lower-cost services exist for streaming, password management, and productivity tools. One useful tactic from r/budget involves using cashback portals, referral codes, and promo codes to reduce the cost of services you're keeping. These micro-savings add up surprisingly fast.

Slash Your Food Budget Without Going Hungry

Food is typically the second or third largest household expense after housing and transportation — and it's one of the most flexible. The gap between what most people spend and what they need to spend on food is significant. The average American household spends roughly $400–$600/month on groceries, plus additional spending on dining out and takeout.

Cooking at home is the highest-impact single habit change you can make on your food budget. A homemade dinner for two costs $5–$12. The same meal at a restaurant costs $30–$60 after tips and drinks. Do that three times a week and you're looking at $75–$150 in monthly savings from one habit shift alone.

Meal planning eliminates food waste, which is one of the most invisible money leaks in most households. Shop with a list, buy ingredients that overlap across multiple meals, and batch cook on weekends when you have time. Buying store brands versus name brands consistently saves 20–30% on groceries without any noticeable quality difference for most staple items like canned goods, pasta, rice, and dairy.

Additional food budget tactics worth implementing:

- Use grocery store apps for weekly digital coupons — many offer $10–$25 in savings per trip when you stack them

- Shop the freezer section for protein — frozen chicken breasts, fish fillets, and ground beef are often 25–40% cheaper than fresh equivalents

- Eat before you grocery shop — hungry shoppers spend measurably more on impulse items

- Pack lunch for work at least three days per week — a packed lunch costs $2–$4 versus $10–$15 for takeout

For anyone on a $20,000 salary or a tight income, food is where the fastest savings typically hide. The goal isn't deprivation — it's spending intentionally on food you actually eat and enjoy.

| Expense Category | Monthly Amount |

|---|---|

| Rent | $1,100 |

| Groceries | $300 |

| Car payment + insurance | $420 |

| Utilities (electric, internet, water) | $180 |

| Phone bill | $80 |

| Health insurance (employee share) | $120 |

| Dining out | $200 |

| Subscriptions (streaming, gym, apps) | $120 |

| Household supplies | $60 |

| Gas / transportation | $120 |

| Savings (target) | $500 |

| Total | $3,200 |

Build Your Emergency Fund First

An emergency fund is the foundation that makes every other savings goal possible. Without one, a single car repair, medical bill, or job disruption wipes out months of progress and often pushes people into high-interest debt that takes years to escape.

The standard recommendation is 3–6 months of essential living expenses. But if that number feels overwhelming right now, start smaller. A $500–$1,000 starter emergency fund is enough to handle most common emergencies without reaching for a credit card. Once you have that buffer, build toward one month of expenses, then three months, then six.

Keep your emergency fund in a liquid, accessible account — your high-yield savings account works perfectly. Don't invest it in the stock market where it could drop 20% right when you need it. The goal is stability and access, not growth. Interest on a HYSA is a bonus, not the point.

Define clearly what counts as an emergency. Car repairs, medical co-pays, job loss, and essential home repairs qualify. A sale at your favorite store does not. This psychological boundary prevents the fund from being raided for non-emergencies — which is the most common way emergency funds disappear.

If you're thinking about longer-term wealth building alongside your emergency fund, the guide on how to build wealth in your 20s covers the full progression from emergency fund to investing to retirement accounts.

Use Clever Ways To Save Money on Every Purchase

Once your budget is set, savings automated, and recurring waste cut, the next layer of acceleration comes from making every purchase work harder. These clever ways to save money don't require sacrifice — they require systems.

Price tracking tools: The Google Chrome browser has a built-in price history tracker — a shopping bag icon that appears on retail sites and shows pricing data over the last 90 days. Many retailers will honor a price drop within 7–14 days of purchase, so checking whether something you just bought dropped in price can result in a refund with a single email. For travel, tools like Google Flights and Skyscanner let you set up email alerts for specific routes so you get notified when fares drop rather than manually checking every day.

Cashback and rewards: Browser extensions that automatically apply cashback at checkout require zero extra effort and consistently return 1–5% on everyday purchases. Stack these with credit card rewards if you pay your balance in full each month. Carrying a balance on a rewards card eliminates any benefit — the interest charges always exceed the rewards earned.

The 24-hour rule: For any non-essential purchase over $30, wait 24 hours before buying. This one habit eliminates a large percentage of impulse purchases. Most of the time, 24 hours later you've either forgotten about it or realized you didn't actually want it. This is one of the most underrated 10 ways to save money that costs nothing to implement.

DIY where the math makes sense: Cutting your own lawn, handling minor home repairs, cooking instead of catering for small events, and doing your own car washing and detailing can save hundreds per year. The key is knowing which tasks have a high hourly savings rate relative to the time they take. A $40 car wash every two weeks is $1,040/year — doing it yourself takes 20 minutes and costs a few dollars in supplies.

Buy used for the right categories: Furniture, tools, exercise equipment, books, and certain electronics hold up well when purchased secondhand. Platforms like Facebook Marketplace and local thrift stores regularly have items at 50–80% below retail. New cars lose roughly 15–20% of value in the first year — buying a certified pre-owned vehicle two or three years old versus brand new is one of the highest-dollar savings decisions a household can make.

For a comprehensive deep dive into the spending-reduction mindset, the frugal living tips guide covers dozens of additional strategies organized by spending category.

How To Save Money Fast: Methods Compared

Not every savings strategy delivers the same speed or impact. The table below compares the most common approaches across three key dimensions so you can prioritize where to focus your energy first.

| Strategy | Monthly Savings Potential | Speed of Impact | Effort Required |

|---|---|---|---|

| Automate savings transfers | $50–$500+ | Immediate | One-time setup |

| Cancel unused subscriptions | $50–$150 | This week | Low (1–2 hours) |

| Cook at home more often | $100–$300 | This month | Medium (habit shift) |

| Build a bare-bones budget | Varies widely | Same day | Medium (1–2 hours) |

| Use cashback and price tracking | $20–$80 | Ongoing | Low (browser setup) |

| Switch to a HYSA | Interest on balance | 30 days to open | Low (one-time) |

| Buy used / DIY maintenance | $50–$200 | Next purchase | Medium (mindset) |

Watch This First

Watch: the Frugal Friends YouTube channel on new money-saving strategies that actually work —

The Frugal Friends YouTube channel covers an angle that most savings guides miss entirely: your online environment shapes your spending behavior. Their insight is that curating what content you consume — specifically, switching from following people who promote buying and lifestyle upgrades to following people who promote saving and intentional spending — changes the baseline desires that drive purchases in the first place. It's a behavioral lever most people never pull.

They also highlight automated price tracking as a genuinely underused tool. Their point is that retailers routinely inflate prices before running a "sale," making it look like you're getting a deal when the price is actually the same as three months ago. Using the built-in price history feature in Google Chrome's browser on shopping sites lets you verify whether a deal is real before clicking buy — a habit that takes seconds and can prevent paying inflated "sale" prices repeatedly.

What Real People Are Saying

In r/Frugal, the most upvoted savings advice consistently points to one thing: automation. Users describe setting up direct deposit splits so a fixed amount goes to a separate savings account before the rest lands in checking. The consensus is that when you never see the money in your spending account, you never miss it — and the savings accumulate without any ongoing effort or discipline.

In r/personalfinance, users regularly point newer savers toward the 50/30/20 framework combined with a high-yield savings account. A common theme in these threads: people who try to save a specific percentage rather than "whatever's left" at month-end are dramatically more successful. The advice to start modest — automating 5% or 10% initially rather than going extreme — comes up repeatedly, with users noting that drastic cuts often backfire within 60 days.

In r/povertyfinance, a recurring piece of advice that doesn't get enough attention: pay off credit cards fully each month, or stop using them entirely. High-interest credit card debt is the single most effective way to destroy a savings plan — it's mathematically impossible to build a meaningful savings balance while carrying a revolving balance at 20–29% APR. Users in this community who made the most progress consistently report eliminating that leak first before anything else.

Frequently Asked Questions

What is the 3 3 3 rule for savings?

The 3-3-3 rule is most commonly referenced in the context of home buying. It requires having 3 months of general living expenses saved as a cushion, 3 months of the new mortgage payment held in cash reserve, and viewing at least 3 comparable homes in person to accurately assess market value before making an offer. For general savings, the more widely applicable rule is 3–6 months of expenses in an emergency fund.

How much can a realistic person save in the first 30 days using these steps?

Most people who complete a budget audit, cancel unused subscriptions, and automate a savings transfer in the same month can free up $200–$500 in their first 30 days. Results vary by income level and starting spending habits — someone with multiple streaming services and frequent dining out has more to cut than someone already living lean. The budget audit alone, for most people, reveals $50–$150 in immediately cuttable expenses.

Is it possible to save money fast on a $20,000 salary?

Yes — though the margins are tighter and the approach must be more deliberate. At $20,000/year (roughly $1,667/month), you have less room for error, which makes a bare-bones budget non-optional. Focus first on keeping housing below 35% of income, eliminating all recurring subscriptions you don't actively use, and cooking virtually all meals at home. Even at that income, consistently saving $100–$150/month is achievable and adds up to $1,200–$1,800 per year. Government assistance programs for food, utilities, and childcare can also free up significant budget room — check eligibility on benefits.gov.

Should I pay off debt or save money first?

Build a small $500–$1,000 emergency fund first. Then aggressively pay down high-interest debt (credit cards, personal loans above 10% APR) before putting significant money into savings. The math is clear: paying off a 24% APR credit card is an automatic 24% guaranteed return, which no savings account or investment can reliably beat. Once high-interest debt is gone, shift that payment amount into savings and investing. If your employer offers a 401(k) match, contribute enough to capture the full match before paying extra debt — it's an immediate 50–100% return on those dollars.

What's the fastest way to save $1,000 starting from zero?

The fastest path to $1,000 combines cutting and earning. Cancel all non-essential subscriptions (frees up $50–$150/month), stop dining out for 60 days (saves $100–$300/month), and add one income stream — overtime hours, selling unused items online, or a short-term side gig. People who attack all three simultaneously typically reach $1,000 within 60–90 days, depending on their income baseline. If you want to accelerate further, the side hustle ideas for beginners guide covers income options that can add $200–$800/month without a second job.

Does the 50/30/20 rule work on a low income?

The 50/30/20 rule is a framework, not a law. On a low income, getting housing, food, transportation, and utilities into 50% of take-home pay may be impossible depending on your location. In that case, modify it to whatever your actual fixed costs are, reduce the "wants" category to 10% or eliminate it temporarily, and save whatever remains — even if it's 5%. A modified 80/10/10 split (80% needs, 10% wants, 10% savings) is more realistic for many low-income households than forcing a 50/30/20 that doesn't fit the math. Also, research from Bankrate consistently shows that starting with any savings habit — even small — is more predictive of long-term financial health than the specific percentage saved.

How do I stop spending money impulsively and start saving instead?

Impulse spending has two main drivers: environment and friction. Remove your credit card information from all saved payment methods in browsers and apps — adding friction to purchases dramatically reduces unplanned spending. Implement a 24-hour waiting rule for any purchase over $30. Unsubscribe from retail email lists and remove shopping apps from your phone's home screen. For deeper behavioral changes, behavioral finance research shows that automation is more effective than willpower — when savings are taken out before you can spend them, the decision is never available to be made impulsively.

Your Next Steps

Understanding how to save money fast is useful. Actually doing it in the next 72 hours is what separates people who build savings from people who keep meaning to. Here's where to direct your energy immediately:

- Today: Pull up your last bank statement and write down your total income and every expense. Identify three subscriptions or recurring charges you haven't used in 30 days and cancel them before you close the browser.

- This week: Open a dedicated savings account — preferably a high-yield savings account at an online bank — and set up an automatic transfer for whatever you can start with, even $50. You can increase it next month. Starting is what matters.

- This month: Cook at home for at least 20 of 30 days. Track every dollar spent against your written budget. At the end of the month, compare what you planned versus what actually happened — that gap is your next target to close.

The people who successfully save money fast aren't more disciplined than everyone else. They've simply built systems that remove the need for discipline. Automate the transfer. Cancel the subscriptions. Write the budget. The hardest part is doing it the first time — every step after that gets easier.

About the Author

Written by Varn Kutser

Personal finance writer covering savings, investing, and budgeting with a data-first approach. Every rate, limit, and claim is verified against official sources — FDIC, IRS, and Federal Reserve. No clickbait, no guesswork, just numbers.

Disclaimer: Rates and terms mentioned in this guide are subject to change. Verify current rates directly with financial institutions before opening any account.

Last updated: April 23, 2026 — fabelo.io